Movies

Localisation drives micro-dramas into the fast lane

60 seconds at a time, a $300 million industry is eating Indian cinema’s lunch — and the real fuel is homegrown stories

MUMBAI: It began with borrowed content. The first wave of micro-dramas washing into India came dubbed from China and Korea, formats transplanted wholesale into a market that was curious but not yet convinced. They grew the audience. They proved the model. And then something more interesting happened: India stopped borrowing and started making its own like there was no tomorrow. Just like their long format show cousins Netflix, Zee5, Amazon Prime, Hotstar (JioHotstar, which recently launched its dedicated ‘Tadka’ micro-drama hub) did a few years ago.

That leap, from imported format to indigenous storytelling, is what has turned micro-dramas from a digital curiosity into an estimated $300 million industry (roughly 2500 crore) in the space of a single year, and what is now driving the next, more explosive phase of growth.

The Velocity of Growth (2024–2030)

| Year | Market Size (Est.) | Growth Rate (YoY) | Industry Milestone |

| 2024 | $45 Million | — | Market Proof: Initial dubbed pilots |

| 2025 | $300 Million | 560% | Localisation: The “Billionaire” becomes the “Zila Parishad” |

| 2026 (P) | $573 Million | 91% | Institutionalization: YRF & Banijay enter |

| 2030 (P) | $4.5 Billion | 31% (CAGR) | Maturity: Parity with niche OTT segments |

Platforms are churning out originals in Hindi, Tamil, Telugu and Bengali. The “Western Billionaire” of the Chinese template is being replaced by the “Zilla Parishad power-player,” the scheming district-level strongman every tier two viewer recognises instantly. Local stories, told in local tongues, are detonating with an energy that no amount of dubbing could ever replicate.

Make in India — Prime Minister Narendra Modi’s pet mantra, or localisation in short — is the engine. Everything else: the technology, the economics, the institutional money piling in, is the vehicle. And the vehicle is moving at supersonic speed.

The micro-drama, a vertically formatted, professionally scripted, episodic series in which each instalment lasts between 60 and 120 seconds, today, according to the Lumikai State of India Interactive Media Report 2025, counts 100 million monthly active users and has racked up more than 450 million app downloads. By 2030, Lumikai projects the market will hit $4.5 billion, at a compounded annual growth rate of 31 per cent. For 2026 alone, a growth rate of 91 per cent is expected. In the attention economy, those are not numbers. They are a declaration of war.

The Platform Leaderboard

| Platform | Key Metric | Core Content Strategy |

| QuickTV (ShareChat) | 50m+ Downloads | Regional depth (Tier 2/3 focus) |

| Dashreels | 2bn+ Episode Views | AI-native, high-velocity production |

| ReelShort/DramaBox | Global Pioneers | High-drama “Billionaire” tropes |

| Amazon miniTV | Scale Aggregator | Free, ad-supported mass reach |

The engagement data is, if anything, more striking than the revenue figures. Micro-dramas already drive a claimed 60 minutes of daily time spent per user, nearly 77 per cent of the levels recorded by established OTT platforms, despite being a fraction of their age. ShareChat and Moj (one of the earliest institutional players to bet on the format) chief business officer Neha Markanda, puts it plainly: the indicators “point toward high monetisation potential, with the format uniquely positioned at the intersection of high engagement and mobile-first storytelling.”

ShareChat’s QuickTV, its dedicated micro-drama product, crossed a claimed 50 million downloads within six months of launch. Together, with Moj, the company states, it now drives over 60 million monthly active users and 400 milion daily episodic plays across the ShareChat ecosystem, with a library of more than 500 original series. (Are your eyes popping out?)

Sixty seconds to hook you; episode four to lose you

The format is engineered for compulsion. A typical series runs 50 to 100 episodes. The first three seconds of each must stop the scroll cold. Episodes one to ten are free. Somewhere between episodes four and seven lies what insiders call the “drop-off zone,” the point at which a weak narrative loses a viewer for good. Survive it, and episode eleven opens the paywall, where real money changes hands. Users purchase “coins” or “tokens” to unlock further episodes, at as little as Rs 5–10 per instalment. The barrier to entry is negligible; the cumulative spend is not. Platforms such as ReelShort, DramaBox and Pocket FM also offer an ad-supported route: watch a 30-second commercial, unlock the next cliffhanger. That model has proved a masterstroke with India’s price-sensitive millions.

On where the monetisation model is headed, Sharlton Menezes, Vice President of IP & Key Partnerships at Pratilipi & Double Tap Films, is measured but clear. “SVOD has seen strong initial adoption, facilitated by the seamless integration of UPI Autopay,” he says. “A balanced mix of ad-supported and subscription revenue will be the primary engine for the industry’s long-term financial health.” The hybrid model, in his reading, is not a compromise. It is the destination.

Unit Economics: Why the Math Wins

| Metric | Traditional OTT Series | Vertical Micro-Drama |

| Cost per Minute | Rs 50,000 – 5,00,000 | Rs 8,000 – 10,000 |

| Production Time | 6 – 12 Months | 3 – 7 Days |

| Discovery | Destination Search | Algorithmic Feed (Scroll) |

| Retention Tool | Star Power | The Cliffhanger |

The economics are ruthless in their efficiency. Producing a micro-drama in India costs approximately Rs 8,000–9,000 per minute of content, a fraction of what a conventional streaming original or even a TV series demands. Artificial intelligence is compressing costs further still, cutting post-production, dubbing and localisation expenses by 20–25 per cent and enabling platforms to release roughly 500 new episodes a month. The return on investment arrives a lot faster than it ever could for a nine-episode web series or a TV series which at times takes six to nine months to start yielding even a marginal profit. For some woebegone TV producers the snip snip happens within three months leaving them with losses in their hands.

But for a clutch of AI-native studios, even those numbers look conservative. Dashverse, a Mumbai-based start-up whose app Dashreels has already clocked two billion episode views, is pushing the cost argument to its logical extreme. Its in-house production tool, Frameo, has cut the bill of producing a show by more than 50 per cent. Dashverse co-founder Lalith Gudipati frames the imperative in clinical terms: “The traditional production model is simply not built to create at the velocity the mobile-first era demands; it is too slow and too resource-heavy.”

Frameo, he argues, enables what he calls a “velocity of imagination” that conventional studios cannot match. The user-behaviour data lends his case some force: Dashreels’ power users are spending a claimed average of 101 minutes per day on the app, and its AI-generated shows are recording episode-completion rates of above 80 per cent, a figure that most long-form streaming platforms would not be embarrassed to claim for an entire season. Dashverse is currently trending at $30 million in annualised recurring revenue and is targeting $100 million by the end of the current financial year.

The big boys smell money

For a long time, micro-dramas were dismissed as the province of scrappy startups and recycled Chinese IP. That era is over. Yash Raj Films, the production house behind some of Indian cinema’s most profitable franchises, is reportedly committing Rs 150 crore to build a micro-drama content slate and a proprietary direct-to-consumer app, a striking pivot for a studio whose identity has been forged on the big screen. Balaji Telefilms, the company that industrialised the Indian daily soap, is collaborating with Vertigo TV to produce premium Hindi vertical dramas, effectively dragging the saas-bahu saga into the smartphone era. When studios of that vintage start chasing a format, the format has arrived.

The institutional disruptor

If Yash Raj and Balaji signal that the gold rush is on, the arrival of Banijay Asia signals something more consequential: that the gold rush is over, and the era of professional-grade, studio-backed vertical television has begun.

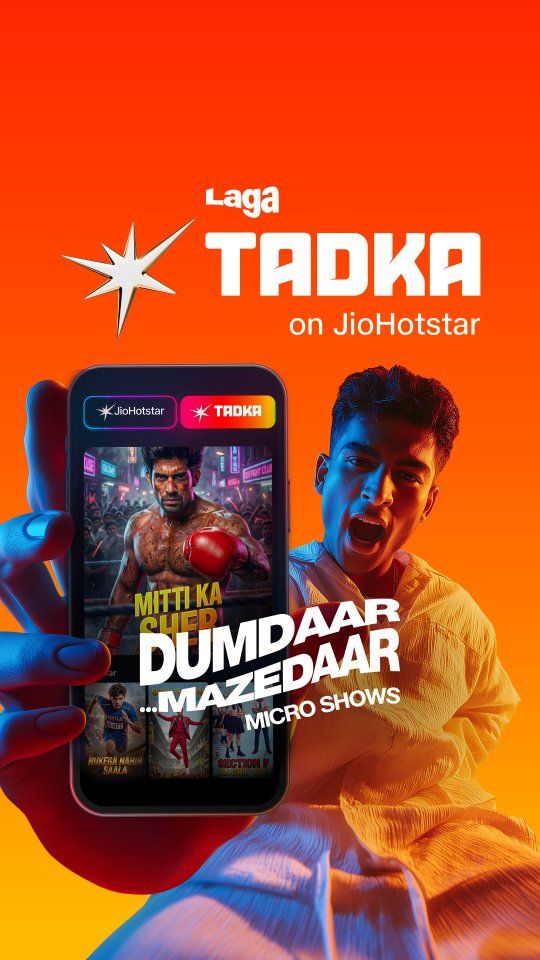

Banijay, the global content group behind some of the world’s most-travelled reality and drama formats, has been laying the groundwork in India since early 2024. The Indian push accelerated sharply in 2026, when the parent company, Banijay Entertainment, used the Series Mania festival (in Lille France) to unveil a dedicated micro-drama slate across its European labels, including Banijay Iberia and Banijay Productions Germany. The Indian division, led by chief executive Deepak Dhar, is now executing what the company frames as a “global-to-local” play of unusual ambition. JioHotstar’s Tadka has launched with 100+ original titles specifically breaking traditional production geographies, moving shoots beyond Mumbai to cities like Indore and Lucknow to unlock regional talent. Notable launch titles include the high-stakes drama Mitti Ka Sher and thrillers like Undercover Boss – Scam Smash

At industry forums including Ficci Frames, Dhar has been unambiguous about his read of the market. “The handheld device is now the primary screen,” he has said publicly, a statement that, from the head of a company whose flagship formats were built for prime-time television, amounts to a reckoning. Banijay Asia is not retrofitting old content for mobile; it is shooting natively in 9:16 vertical format from the first frame.

Its competitive positioning is clever. Rather than chasing the “billionaire romance” lane that ReelShort and DramaBox have colonised, Banijay is leaning into its core strength: high-stakes, high-emotion unscripted and reality content. Around its flagship formats for JioHotstar and Prime Video, The Fifty and The Alliance, it is building what it calls “vertical wraparound” micro-series: 60–90 second narrative extensions that offer behind-the-scenes access or alternate-perspective storylines, keeping audiences tethered to an IP between main episodes. It is, in essence, using the micro-drama as a loyalty mechanism rather than a standalone product.

Banijay is also adapting a model already tested by its German label, which launched a 28-episode micro-drama headlined by creators commanding a combined following of 33 million. In India, the company is reportedly developing a creator-centric universe that partners social-media influencers as on-screen talent, bypassing traditional marketing entirely and tapping directly into the “scroll-to-watch” habit that drives 89 per cent of micro-drama discovery through social feeds, according to a 2026 report by Meta and Ormax Media.

Quality is the other lever. While the micro-drama category has been plagued by cheap-looking content, Banijay is deploying the production infrastructure of its Endemol Shine India operation to hold costs at Rs 8,000–10,000 per minute while maintaining the lighting and sound standards of prestige OTT productions such as The Night Manager. It is also translating proven European scripts, including the darkly comic Fcking Honeymoon, for Indian casts and contexts, compressing the development cycle dramatically. And rather than building its own destination app, the company is positioning itself as a content factory for others, in discussions with short-video platforms Moj and Josh as well as the mini-TV arms of major streamers, supplying high-retention vertical drama that keeps users on third-party platforms longer.

Menezes, who has watched the category evolve from the front row, sees the next chapter clearly. “The category initially launched with significant momentum, seeing over 20 players competing for market share,” he says. “With the entry of major conglomerates, the landscape is ripe for consolidation. We anticipate a market correction where long-tail incumbents primarily reliant on high cash-burn strategies will likely exit.” The platforms that survive, in his view, will be those with the content depth and distribution muscle to outlast the shakeout.

An accidental audience

A peculiar tailwind has accelerated all of this. India’s 2025 crackdown on real-money gaming apps left tens of millions of users suddenly short of a way to spend 45 idle minutes on their phones. Lumikai’s analysis suggests a significant portion of that displaced time-share migrated directly to micro-dramas and audio platforms, an involuntary subsidy to an industry that was already growing at pace. The gamer became the binge-watcher; the leaderboard became the cliffhanger.

Audience Breakdown: The Indian Exception

| Segment | Global Trend | The India Reality |

| Gender Split | Overwhelmingly Female | 70% Male |

| Geography | Metro/Urban | 60% Tier 2 & 3 Cities |

| Genres | Billionaire Romance | Revenge / Action / Supernatural |

| Usage Time | 30-40 mins / day | 60-100 mins / day |

The resulting audience confounds global expectations. Worldwide, the “billionaire romance” genre draws an overwhelmingly female viewership. In India, nearly 70 per cent of micro-drama users are male, drawn instead to revenge narratives, underdog-success arcs and supernatural action. More than 60 per cent come from tier two and tier three cities, where mobile data is the primary, and often only, conduit to the wider entertainment world. Users are spending a median of 3.5 hours a week on these platforms, typically in seven or eight short sessions a day, peaking between 8pm and midnight.

Menezes flags a genre problem brewing beneath the headline numbers. “The romance genre, specifically billionaire and CEO tropes, is heavily over-indexed across platforms,” he says. “While these themes have performed exceptionally well to date, audience fatigue is inevitable. There is a strategic need for platforms to diversify their content slates and increase production budgets to explore more sophisticated and varied genres.” The warning is directed at platforms still doubling down on a formula that built the market but may not sustain it.

Speaking in tongues

The first wave of micro-dramas leaned heavily on dubbed Chinese and Korean content. The second wave is emphatically homegrown. Platforms are now churning out originals in Hindi, Tamil, Telugu and Bengali, localising archetypes with surgical precision: the “Western Billionaire” of the Chinese template is being replaced by the “Zilla Parishad power-player,” the scheming district-level strongman every tier two viewer recognises instantly. The result, platforms report, is a threefold improvement in retention in non-metro markets.

Menezes is unequivocal on why. “Original local content is the real differentiator,” he says. “With nearly 60–70 per cent of viewers originating from tier two and tier three cities, relatability is paramount. Local stories, nuanced cultural contexts and native dialects resonate far more deeply than dubbed imports, a trend we have seen proven across almost every other media format in India.” While the industry has been predominantly Hindi-centric, Menezes believes the next phase of growth will be driven by regional expansion. “Tapping into local language audiences is essential to capturing the next wave of diverse Indian viewers,” he adds.

Data-led outfits such as Pratilipi, via its Double Tap Films venture, are mining libraries of millions of web-novel readers to identify which stories carry a pre-validated audience before a single frame is shot. Traditional platforms are paying attention too. MX Player and Amazon miniTV are both quietly incorporating micro-drama-style content to retain the 18–24 demographic they fear losing to nimbler rivals.

ShareChat’s Markanda believes the next phase of expansion will be driven by three forces: “deeper regional storytelling, creator-led studios and faster, tech-enabled production cycles.”

The framing is precise. Regional storytelling addresses the language gap. Creator-led studios dissolve the boundary between marketing and content. And accelerated production cycles, the point at which AI and lean infrastructure converge, make the whole enterprise self-sustaining at scale.

Dashverse’s Gudipati, whose platform is targeting a super optimistic production of more than 500 shows a month by the second half of 2026, sees the same horizon from a different vantage point. The micro-drama’s central insight, he argues, is that dopamine and depth are not opposites. “The magic of the microdrama format lies in its ability to marry that high-frequency gratification with deep, serialised storytelling that keeps users hooked episode after episode.” The format, in other words, is not a concession to shortened attention spans. It is an exploitation of them.

The interval is over

What micro-dramas have accomplished, in the space of barely two years, is the construction of an entirely new consumption layer in Indian entertainment. As Markanda puts it, the format is “moving users from passive scrolling to active, episodic viewing,” occupying the space between the disposable ten-second clip and the immersive long-form series, a gap that nobody knew existed until it was filled.

Mithilesh Bhagat, founder of Tamasha Studios emphasizes, “Micro-content has existed before, but it has not been backed by an ecosystem that can drive both discovery and consistency at this level.” Firdaus Sayed, partner at Salt Media adds that the format is “opening up content creation… allowing storytellers across sizes to participate without being constrained by large budgets.”

The start-ups proved the model. The AI studios turbocharged the economics. The legacy houses validated the cultural weight. Now JioHotstar, with its ‘Tadka’ hub, and players like Banijay are betting that good formats travel vertically too. And the traditional gatekeepers of Indian entertainment, the multiplexes, the prime-time broadcasters, the subscription streaming giants, are watching a Rs 2,500 crore market that did not exist three years ago and recalibrating, urgently, what the word “screen” even means anymore.

The interval, in every sense, is over.