News Broadcasting

Star News asserts it is real No. 2; claims lead position among affluent males

MUMBAI: The scrap for pole position in the Hindi news channel space may still be a while away with Aaj Tak the clear leader, but where the action is right now is for the Number 2 slot.

In clear riposte to NDTV India stating to Indiantelevision.com recently that it was now the Number 2, chief rival Star News has issued a counter. A company release asserts that it is in fact the number two channel among the the key C&S, 25+, male, SEC ABC demographic, in the Hindi speaking markets.

Going one further, it states that among SEC A males 25+ it is ahead even of Aaj Tak (data for six main metros, including Delhi and Mumbai).

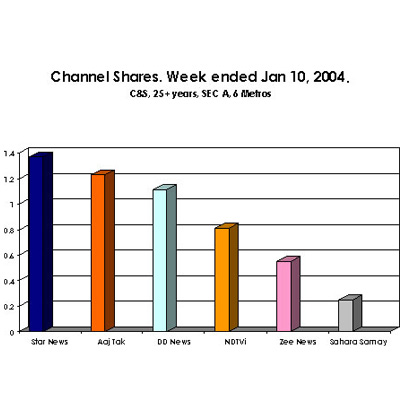

The data refers to the latest TAM figures for the week ending 10 January 2004 and average channel shares for the past four weeks.

Backing up its claim to being the favourite news channel for the upmarket adult male, the release quotes channel shares for the week 4 – 10 January 2004 in C&S, 25+ years, SEC A, 6 metros that show it ranks first with 1.37, followed by Aaj Tak 1.23, DD News 1.11 and NDTV India coming in a lowly fourth with 0.81

Jan 4 – 10 4 week avg

Aaj Tak 2.9 3.04

Star News 1.34 1.37

NDTV India Hindi 1.28 1.36

Zee News 1.14 1.23

DD News 0.88 0.92

Sahara Samay 0.49 0.60

(TG: Male 25+, SEC ABC – Hindi Speaking Markets)

Commenting on the performance, president & CEO of Star News Ravina Raj Kohli is quoted in the release as saying, “The latest figures reaffirm that Star News is one of the fastest growing Hindi news channels and the most preferred channel among urban viewers in SEC A homes across six metros. This is a tremendous achievement for a young news channel.”

Two channels both claiming the Number 2 position? Indiantelevision.com asked TAM to do a run through the data that had been supplied and this is what the reply was – both seemed okay but there might be some slight differences as to the Hindi-speaking markets covered in the two sets of data that have been issued.

Further, NDTV’s data was for the period between 7 December 2003 and 3 January 2004 while Star News is more recent and covers a four-week period up to the week ending 10 January. NDTV’s data had three time bands covered – all day (24 hours), evening prime (6 pm to midnight) and morning prime (6 am to 9 am). Star News did no time band break ups and the data represents absolute channel shares (all day) over four weeks.

What this seems to indicate is that, as of now, the two channels are running virtually neck-and-neck. It may well be the coming general elections that delivers a clear verdict on the Number 2. But for the moment it looks like a “hung result”.