MAM

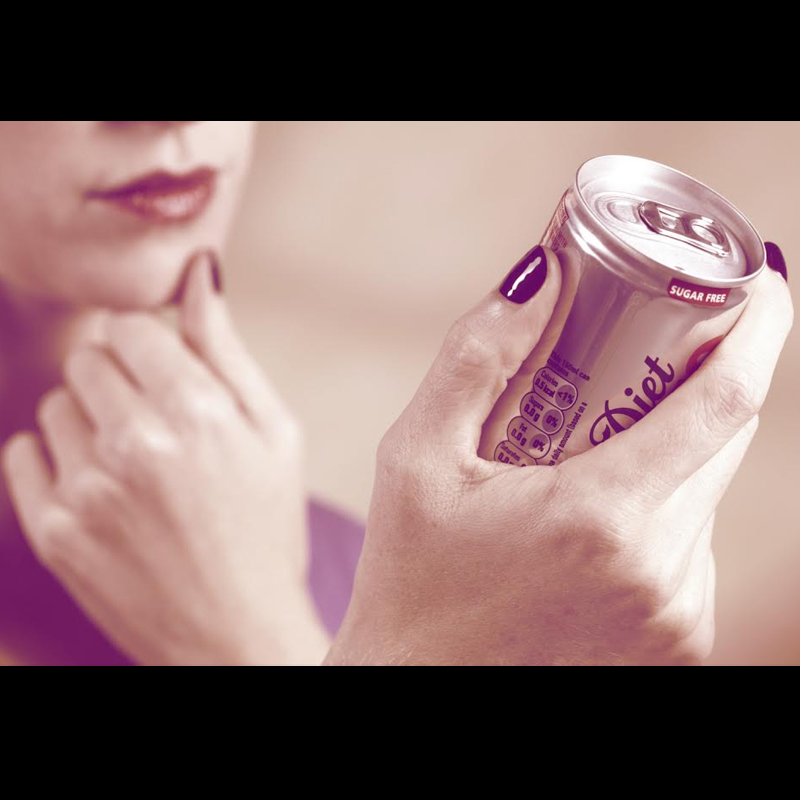

Should Coca-Cola pull the plug on Diet Coke?

MUMBAI: Diet soda seems to be a dying beverage breed. Despite having been around for the longest time in the market, diet sodas fallen out of favour with consumers and redemption isn’t in sight. Ever since carbonated drinks hit the market, countless inventors, entrepreneurs and engineers have tried to enhance the taste, flavour and packaging of the product while also trying to reduce the sugar content.

The beginning of the diet refreshment was in 1952, when Kirsch Bottling in Brooklyn, New York launched a sugar-free ginger ale called No-Cal, which was designed for diabetics, not dieters, and distribution remained local. In 1962, American soft drink company, Dr Pepper released a diet(etic) version of its soft drink, although it sold slowly due to the misconception that it was meant solely for diabetic consumption.

It was only in 1963 when Coca-Cola saw the power and joined the diet soft drink market with Tab, which proved to be a huge success.

Pepsi entered in the segment with Patio Diet Cola in 1963 and renamed it as Diet Pepsi the following year. Diet 7 Up was released in 1963 under the name Like but was soon discontinued in 1969 due to the United States government ban of cyclamate sweetener. After its reformulation and renaming it to Diet 7 in 1979, Coca-Cola countered this by releasing Diet Coke in 1982. After the release of Diet Coke, Tab took a backseat on the Coca-Cola production lines as Diet Coke could be more easily identified by consumers.

According to researches, many people turn to diet carbonated soda believing these would be a healthy alternative to sugary drinks or alcohol. But, several reports have revealed that aerated drinks actually cause people to feel empty which further leads them to over eating. This is primarily due to high levels of carbon dioxide present in these drinks that trigger a hunger hormone called ghrelin.

The global multinational beverage company Coca Cola recently launched a £10 million (Rs 90.4 crore) ad campaign to commence a refreshed packaging for Diet Coke along with two new flavours, Exotic Mango and Feisty Cherry.

The brand is banking on millennials who don’t drink Diet Coke to turn around the fortune of the struggling soda brand.

Coca Cola CEO James Quincey isn’t completely satisfied with Diet Coke’s performance and the introduction of new flavours and the new revamped identity is a desperate attempt to gain some lost market share. “One of our points of dissatisfaction in 2017 was that we were not about to turn around Diet Coke. We hope to find a path forward for Diet Coke, and at the very least stop declining sales.”

The new flavours and packaging, Quincey says are a step in the right direction, but they may not be enough to actually increase Diet Coke sales.

With an emphasis on millennials, the revamp and experimentation is targeted to those who don’t regularly drink Diet Coke. For the last few years, Diet Coke has been the weakest link in Coca Cola’s lineup despite being a zero-calorie drink and has struggled to win over many health-conscious shoppers.

People across the globe are increasingly cutting out sugar from their diet. The market of diet sodas in the US has dropped by a whopping 34 per cent since 2005 and the US industry beverage digest reported a sales drop in Diet coke’s portfolio by 1.9 per cent in 2016.

In India, Diet Coke and Diet Pepsi failed miserably. Although the products were launched with much fanfare, they were not able to capture any market share and Pepsi decided to pull the plug on the Diet variant. Similar was the fate of Diet Coke.

Another reason for the products’ failure could be its peculiarly artificial taste that due to less sugar content.

The distribution aspect has been another roadblock for the company as the concept of diet soda continues to remain unpopular and unknown in rural segments of India.

But with the new revamped brand identity and introduction of new flavours which might hit the Indian market soon, Coca Cola is hoping for better days ahead as it still continues to be one of the largest beverage manufacturers globally and Thums Up is the most consumed aerated drink in India.

Also Read :

Kids’ candy segment: Communication sees a shift

Should junk food ads be banned on kids’ channels?

Guest Column: The future of advertising

Digital

Content India 2026 opens with a copro pitch, a spice evangelist and a £10,000 prize for Indian storytelling

Dish TV and C21Media’s three-day summit puts seven ambitious projects before an international jury, and two walk away with serious development money

MUMBAI: India’s content industry gathered in Mumbai this March for Content India 2026, a three-day summit organised by Dish TV in partnership with C21Media, and it wasted no time making a statement. The event opened with a Copro Pitch that put seven scripted and unscripted television concepts before an international panel of judges, and by the end of it, two projects had walked away with £10,000 each in marketing prize money from C21Media to support development and international promotion.

The jury, comprising Frank Spotnitz, Fiona Campbell, Rashmi Bajpai, Bal Samra and Rachel Glaister, evaluated a shortlist that ranged from a dark Mumbai comedy-drama about mental health (Dirty Minds, created by Sundar Aaron) to a Delhi coming-of-age mystery (Djinn Patrol, by Neha Sharma and Kilian Irwin), a techno-thriller about a teenage gaming prodigy (Kanpur X Satori, by Suchita Bhatia), an investigative crime drama blending mythology and modern thriller (The Age of Kali, by Shivani Bhatija), a documentary on India’s spice heritage (The Masala Quest, hosted by Sarina Kamini), a documentary on competitive gaming (Respawn: India’s Esports Revolution, by George Mangala Thomas and Sangram Mawari), and a reality-horror competition merging gaming and immersive fear (Scary Goose, by Samar Iqbal).

The session was hosted by Mayank Shekhar.

The two winners were Djinn Patrol, backed by Miura Kite, formerly of Participant Media and known for Chinatown and Keep Sweet: Pray & Obey, with Jaya Entertainment, producers of Real Kashmir Football Club, also attached; and The Masala Quest, created and hosted by Sarina Kamini, an Indian-Australian cook, author and self-described “spice evangelist.”

The summit also unveiled the Content India Trends Report, whose findings made for bracing reading. Daoud Jackson, senior analyst at OMDIA, set the tone: “By 2030, online video in India will nearly double the revenue of traditional TV, becoming the main driver of growth.” He noted that in 2025, India produced a quarter of all YouTube videos globally, overtaking the United States, while Indians collectively spend 117 years daily on YouTube and 72 years on Instagram. Traditional subscription TV is declining as free TV and connected TV gain ground, forcing broadcasters to innovate. “AI-generated content is just 2 per cent of engagement,” Jackson added, “highlighting the dominance of high-quality human content. The key for Indian media companies is scaling while monetising effectively from day one.”

Hannah Walsh, principal analyst at Ampere Analysis, added hard numbers to the picture. India produced over 24,000 titles in January 2026 alone, with 19,000 available internationally. The country now accounts for 12 per cent of Asia-Pacific content spend, up from 8 per cent in 2021, outpacing both Japan and China. Key exporters include JioStar, Zee Entertainment, Sony India, Amazon and Netflix, delivering over 7,500 Indian-produced titles abroad each year. The top importing markets are Saudi Arabia, the UAE, Egypt, the United States and the Philippines. Scripted content dominates globally at 88 per cent, with crime dramas and children’s and family titles performing particularly strongly.

Manoj Dobhal, chief executive and executive director of Dish TV India, framed the summit’s ambition squarely. “Stories don’t need translation. They need a platform, discovery, and reach, local or global,” he said. “India produces more movies than any country, our streaming platforms compete globally, and our tech and creators win international awards. Yet fragmentation slows growth. Producers, platforms, and tech move in different lanes. We need shared spaces, collaboration, and an ecosystem where ideas, technology, and people meet. That is why we built Content India.”

The data, the pitches and the prize money all pointed to the same conclusion: India is not waiting for the world to discover its stories. It is building the infrastructure to sell them.