MAM

Myntra endorses hassle-free returns in latest campaign

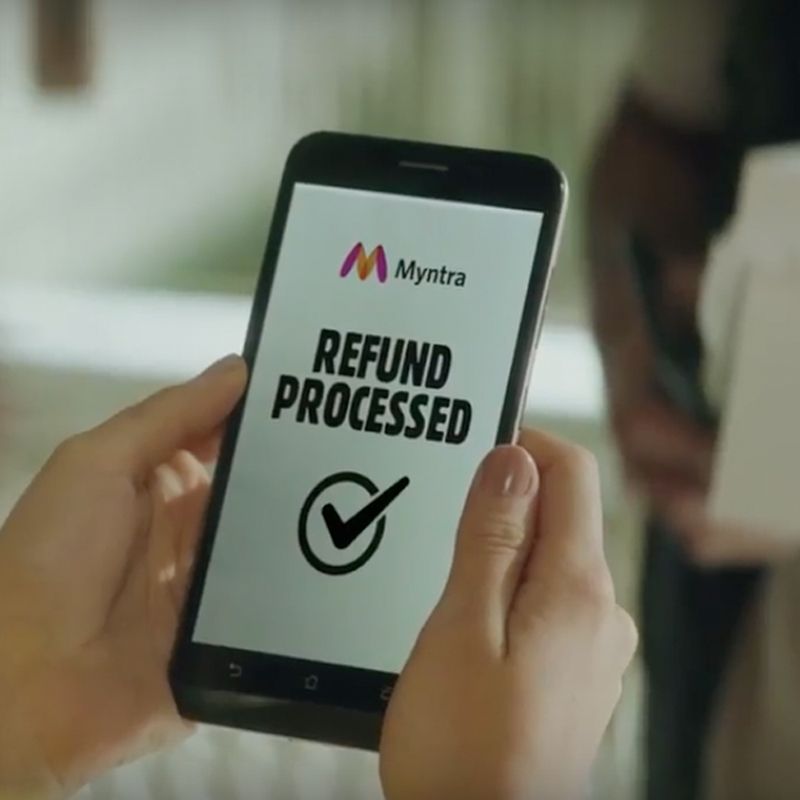

MUMBAI: Fashion e-commerce site Myntra is wooing new customers, people who have never shopped online, from non-metro cities and smaller towns. The marketing campaign will focus on pain points such as seamless returns and instant refunds, which inhibit them from taking the online leap. The TVCs have been conceptualised by Taproot Dentsu.

Commenting on the campaign, Jabong head and Myntra CMO Gunjan Soni said, “Non-metro cities are very important markets for Myntra as we see our next phase of growth coming from there. Our research shows that over 30 million SEC A internet users in non-metros do not shop online and, as a market leader, we have launched this campaign to drive adoption among them. We see about 25 per cent of our daily acquisitions coming from this segment. With this campaign, we are looking at acquiring half a million new customers from this target group over the next three weeks.”

One of the TVCs features Dangal star Fatima Sana Shaikh as she threatens the Myntra delivery boy with dire consequences if the refund money gets stuck in the process. To this, he says that she can be assured of instant refund at Myntra. The second TVC talks about how someone can go to a great extent to convince a person the shirt doesn’t fit well and so needs to be returned. The Myntra executive says it has a no-questions-asked return policy.

Taproot Dentsu creative director Neeraj Kanitkar said, “Myntra is undisputedly one of India’s most fashionable shopping outposts. But some shoppers, especially from non-metro cities, worry about the practicalities of the service features. Will my return be accepted? Will my return have to meet any requirements? When will I get a refund? And as a result simply stay away from shopping for fashion online. This campaign addresses these questions in a thoughtful, warm yet joyful manner. Which will hopefully get them to try Myntra because once people try Myntra, they really do love it.”

The campaign will use other mediums like TV, digital, online and outdoor as well.