Hindi

PVR-Inox deal: Consolidation to boost in-cinema advertising; steer advertiser segmentation for industry

Mumbai: The all-stock merger between two of the country’s largest multiplex chains PVR and Inox Leisure announced earlier this week has been reckoned as positive for the industry on all counts. Led by PVR’s Ajay Bijli as MD, the combined entity PVR-Inox will have an invincible size advantage with its 1546 screens across 341 in 109 Indian cities, against Carnival and Cinepolis’ nearly 400 screens.

Meanwhile, Kanakia Group-owned Cineline India has announced to re-enter the business after a decade in Q1FY23 with a total of 75 screens, of which 27 were acquired in February.

Valued at 30-45 per cent higher than standalone entities Inox (~Rs 64 billion) and PVR (~Rs 110 billion), PVR-Inox will have a screen share of over 50 per cent within India multiplexes and 18 per cent within overall screens. Its combined box office share for Hindi and English content, which has a 65 per cent share in the overall box office, will be around 42 per cent, as per Elara Securities.

Gaining from Premiumisation

Weakening dynamics for the unorganised and single-screen film exhibition players, even before the pandemic hit, presented a tremendous opportunity for the organised ones to increase their foothold in the segment.

Consolidation in the film exhibition sector started around 2014-15 with the buyout of Satyam Cineplex by Inox for Rs 240 crore, and Carnival’s mop-up of HDIL’s Broadway Cinemas for Rs 110 crore. In December 2014, Reliance Capital sold its multiplex business of Reliance MediaWorks (RMW) operating under the brand name ‘Big Cinemas’ to Carnival Cinemas for Rs 700 crore. The following year Mexican multiplex chain Cinepolis acquired Essel Group’s Fun Cinemas and PVR bought out DLF’s DT Cinemas for Rs 500 crore.

Cineline India, which was present in the trade as Cinemax since 1997, sold its multiplex business along with Cinemax brand to PVR for Rs 395 crore under a non-compete clause in 2012. In light of the deal’s expiration on 31 March, the company is set to re-enter the business in the first quarter of FY’23.

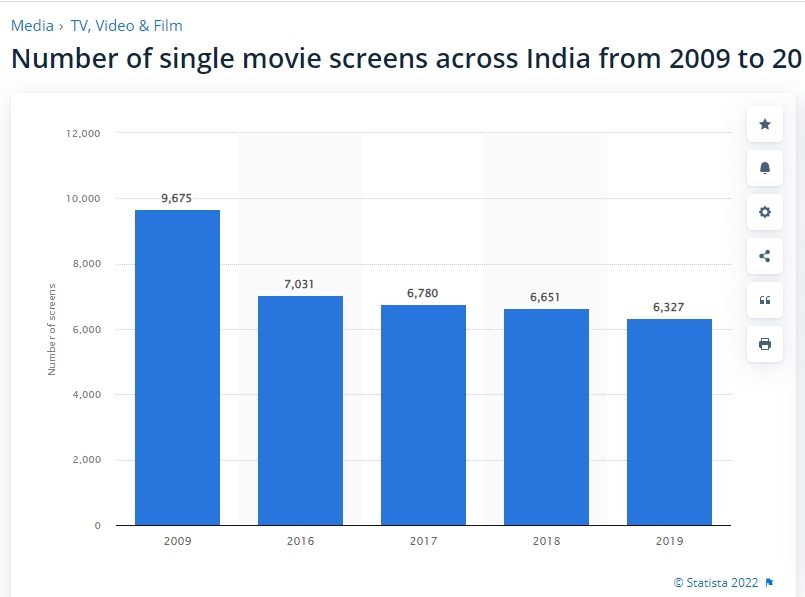

From 9,600 screens in 2009, single cinema screens were reduced to just over 6,300 by 2019 in India. This decline is reflected in the country’s screen density which stood at 74 in 2019 (Statista). At an estimated overall screen count of 9,423 (FICCI-EY, March 2022), India is a largely underscreened country as compared to China which has around 70000 screens for comparable population size. Its ATP (Average Ticket Price) and SPH (Spends Per Head) are also among the lowest. Bridging the demand-supply gap in the Indian exhibition industry is expected to increase the box office collections by more than three times, as per Delloite’s 2018 report on screen density.

Even as the economies of scale usher in revenue and cost benefits, rapid premiumisation in cinematic and customer experience led by technologies like 3D, 4DX, Imax, F&B, and other luxury offerings, as well as Covid-mandated hygiene standards, will drive ATP and SPH on one hand, and create more and better opportunities for advertisers on the other, thereby boosting advertising revenues for the new entity, and consequently for the industry at large.

The merger will help in getting higher SPH (Rs 99 for PVR vs Rs 80 for Inox in FY20) on existing Inox screens. In FY ’20, Inox’s footfall of 6.6 crore gave additional F&B revenue of ~Rs 125 crore and net cost revenue of more than Rs 90 crore. The synergies may also result in substantial savings on manpower costs. On combined manpower costs of over Rs 600 crore, even a 20 per cent saving will result in savings of Rs 120 crore for the combined entity. Overall, the merger has the potential to add over Rs 300 crore to the bottom line of the combined entity, digital cinema distribution network and in-cinema advertising platform, UFO Moviez tells IndianTelevision.com.

Boost to in-cinema advertising

Last October as theatres began to reopen after 18 months of strict and partial lockdowns, in-cinema advertising which contributes 10-12 per cent to the overall revenue pie for cinemas, witnessed a slump of 25-30 per cent in rates. Studying the trend, Inox Leisure chief sales and revenue officer Anand Vishal had previously told IndianTelevision.com that “cinema is not going to be an easy sell” for quite some time hereafter.

Cinema is not going to be an easy sell: Inox’s Anand Vishal

This merger is expected to turn the tables in favour of the exhibitors sooner than previously estimated. According to UFO Moviez “the consolidation will be positive for overall in-cinema advertising in the country. In FY ’20, PVR was earning ad revenue of ~Rs 45 lacs per screen whereas Inox was at ~Rs 28.5 lakh, a difference of nearly Rs 17 lakh per screen. The combined entity should be able to get the same revenue as PVR for all screens. Thus, on around 650 screens of Inox, differential ad revenue of Rs 17 lakh per screen will translate into additional ad revenue of ~Rs 110 crore for the combined entity.”

The segmentation of advertisers between big and smaller chains/single screens, which already existed by virtue of the players having differentiated TGs, will become more pronounced going forward.

“PVR and Inox together have screens in around 110 cities whereas UFO has ad rights of over 3500 screens (smaller chains/single screens) spread across close to 1400 cities and towns. An advertiser/agency will now be required to deal with only two entities to advertise on a pan India network spread over 5000 screens. This will help in minimising admin work, which in turn will lead to faster closure of deals,” UFO Moviez observes.

In spite of being among the hardest hit, the cinema exhibition industry is staging a phenomenal recovery with the success of films like “The Kashmir Files,” “RRR” and “Gangubai Kathiawadi.”

dentsu Creative India CEO Amit Wadhwa points out that while “brands may have been circumspect regarding the above investments, in-cinema advertising will pick up henceforth, especially with the two big names coming together to form a much stronger brand. It has the possibility of creating better opportunities for brands to advertise and hence, in the bargain, the likelihood of charging a premium.”

On the contrary

Even though the “onslaught of OTT” has been ostensibly stated as the reason, the PVR-Inox merger was always on the cards. The surge in OTT consumption as a result of the pandemic may have only expedited it. As film producer Naveen Chandra opines, “We are in the initial stages of OTT growth in India so any responsive strategies based on the binging nature of consumers may be premature.”

Commenting on its likely impact on distribution, he adds, “Any business that scales up to a near majority market share will have an advantage of charging a pricing premium for its products. The combined entity will hold nearly 60 per cent of the multiplex screens. That’s a great advantage whichever way you look at it. The programming muscle it provides is phenomenal as the entity negotiates its exhibition deals or exclusive release windows with platforms or theatrical shares with producers.”

Irrespective of the assertions and speculations, OTT players have considered Cinemas an enabler rather than a competitor, even in the context of ‘windowing’ which became a ‘hot potato’ for the industry and media in the last couple of years.

OTTs to benefit from the availability of price discovery platform as cinemas reopen

Shemaroo Entertainment COO Kranti Gada asserts that “right from providing a barometer to assess a film’s worth, to unclogging the pandemic-paused film pipeline, and saving marketing costs for streaming platforms, the growth of cinemas will only be beneficial for OTT platforms.” Shemaroo Entertainment owns the video-on-demand service ShemarooMe.

While OTTs are being projected as the eventual replacement of single screens, affordable cinema is here to stay, players and observers agree. The Southern anomaly where PVR and Inox hold six and three per cent share respectively stands testimony to it.

Hindi

GUEST COLUMN: Why film libraries & IPs are the new engines of growth

Unlocking value through catalogue strength and IP synergy

MUMBAI:In a media landscape defined by fragmentation, platform proliferation, and ever-evolving audience behavior, the economics of filmmaking are undergoing a fundamental shift. No longer confined to box office performance, a film’s true value is now measured across an extended lifecycle that spans digital platforms, syndication networks, and global markets. As content consumption becomes increasingly non-linear and algorithm-driven, film libraries and intellectual properties (IPs) are emerging as strategic assets, capable of delivering sustained, long-term returns. For Mohan Gopinath, head – bollywood business at Shemaroo Entertainment Ltd., this transformation signals a decisive move from hit-driven models to portfolio-led value creation. In this piece, Gopinath explores how legacy content, when intelligently repurposed and distributed, can unlock recurring revenue streams, why the interplay between catalogue and original IP is critical, and how media companies can build resilient, future-ready entertainment businesses.

For all these years, we thought that a film is successful if it performs well in theatres. There are opening weekend numbers, box office milestones, and distribution footprints that gave a good picture of how the movie has done commercially and also tell us about its cultural impact. However, there are multiple platforms today, always-on content ecosystem, which has caused a shift. Today, the theatrical performance is not the culmination of a film’s journey but merely the beginning of a much longer and more dynamic lifecycle.

Film libraries today are emerging as high-value, constantly evolving assets that deliver sustained returns well beyond initial release cycles. This becomes a point of great advantage for legacy content owners with diverse catalogues, to shape long-term business outcomes.

According to FICCI-EY, the media and entertainment industry of India achieved a valuation of Rs 2.78 trillion in 2025 which is expected to reach Rs 3.3 trillion by 2028 through a compound annual growth rate of approximately 7 per cent and digital media will bring in more than Rs 1 trillion to become the biggest sector which generates about 36 per cent of overall market revenues.

This shift is the expansion of distribution endpoints. We know how satellite television was once the primary secondary window but today, it coexists with YouTube, OTT platforms, Connected TV, and FAST channels. Each of these platforms caters to distinct audience demographics and consumption behaviors, helping content owners to obtain more value from the same asset across multiple formats.

For instance, films that had great reruns, now find continuous engagement across digital platforms. On YouTube, classic Hindi cinema continues to attract significant viewership, reaching audiences across generations and geographies with remarkable consistency. At Shemaroo Entertainment, this is reflected in our film library shaped over decades as part of a long association with Indian entertainment. From classics such as Amar Akbar Anthony to much-loved entertainers like Jab We Met, Welcome, Dhamaal, Phir Hera Pheri, Dhol, Golmaal, and Bhagam Bhag, many of these titles continue finding new audiences while retaining their place in popular memory. Their enduring appeal reflects how culturally resonant stories can continue creating value over time. Similarly, FAST channels have created curated, always-on environments where catalogue content can continue to thrive through star-led and genre-based programming.

This multi-platform approach has very well transformed films into long-tail IP assets which are capable of generating recurring revenue across advertising, subscription, and syndication models.

The evolution of audience behavior is equally important. Nowadays, it’s more important to find what’s more relative than what’s recent as viewers are more influenced by mood, memories, and algorithmic suggestions than by release schedules. Even if a movie was released decades ago, it can trend alongside a newly released movie, if surfaced in the right context. Thoughtful packaging, whether through festival-based playlists, actor-driven collections, or genre clusters, allows catalogue content to remain dynamic and continuously discoverable. Shemaroo Entertainment has built extensive film libraries over decades and its focus has mostly been on recontextualizing content for the consumption of newer environments. This process doesn’t just include digitization and restoration, but also re-packaging of films as per platforms.

Syndication itself has evolved into a key growth driver. In perspective, when looking at the domestic market, curated content packages continue to find strong demand across broadcast and digital platforms. Meanwhile, in the international market, especially in markets like Middle East, North America and Southeast Asia, the appetite for Indian content is opening up new monetization avenues. Here, the ability to package and position catalogue content effectively becomes as important as the content itself.

Importantly, the need to re-package catalogue content does not diminish the role of new content. In fact, originals and fresh IP are essential to sustaining the long-term value of a film library because they act as discovery engines that bring audiences into the ecosystem, while catalogue content drives depth, retention, and repeat engagement.

This interplay between the “new” and the “known” is what defines a robust content strategy today. While new films generate spikes in consumption, catalogue titles offer familiarity and comfort. These are factors that are increasingly valuable in an era of content abundance and decision fatigue. This is also shaping our strategy, drawing value from both a deep catalogue assets and a growing focus on original IPs to strengthen long-term audience engagement and build more predictable revenue streams.

There is growing recognition that long-term value in entertainment will be shaped not only by how intelligently existing content continues to live, travel and find relevance, but also by how consistently new stories are created to renew that ecosystem. In that sense, film libraries and original IP are not parallel bets, but reinforcing engines of growth. For media companies, the opportunity lies in making these two forces work together, because that is increasingly where more resilient and predictable businesses are being shaped.

Note: The views expressed in this article are solely the author’s and do not necessarily reflect our own.