MAM

Post-lockdown perceptions, aspirations and anticipations of Indian millennials

MUMBAI: The current lockdown is a dark phase, something that the world has not witnessed in decades. But there is always a silver lining in any adverse situation. Laqshya Media Group has found a bit of that silver lining by conducting a research study to help marketeers figure out the perceptions, aspirations and anticipations of the Indian Millennial via-a-vis the ‘New Normal’ that the world faces today.

An online study was conducted reaching 1104 respondents across the primary cities in India. The target group belonged to the age group between 18 and 39, across genders and representing both NCCS A andB. Summarising all the reports and survey results has helped Laqshya assess the perceptions, aspirations and anticipations of the Indian millennials. The good news is that not only are the IMF and the RBI confident of India bouncing back – so are the Indian Millennials. A few findings of the report are excerpted below.

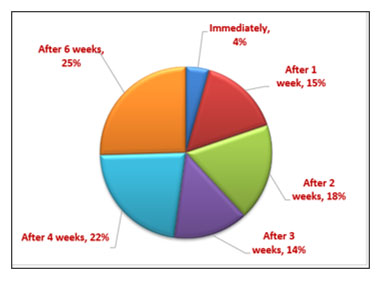

The research talks about customer behavior as per two primary age groups 18-25 and 26-39. Analysis shows that each cohort responded differently to some of the questions posed to them, while they were statistically similar in response to others. For example, one of the questions was whether people will wait to visit malls, restaurants or any public places right after the lockdown is lifted. 75 per cent of the entire respondent base responded that they will be back within four to five weeks. The younger people, 18-25, shared that they will hit the malls in an average of 23 days while the 25-39 cohort’s average wait time was 29 days!

But 31 per cent of the targeted group is more likely to use personal travel more frequently as compared to earlier. A sneak peak of this data can be seen in the pie chart given below that shows the time people will wait to go out post the lockdown.

It is interesting to realise that people have different mindsets towards outings, investing and traveling. Similar to the aforementioned question, a series of questions were asked to the people from different ages, genders, backgrounds and professions. Majority of people responded that they want to meet friends and family after the lockdown. It was noted that younger people and women had a major inclination towards eating out.

The millennials are optimistically cautious especially in investing money or procuring assets. 53 per cent of the respondents want to invest in fixed deposits, but more than 40 per cent of them continue to have faith in mutual funds, and more than a quarter anticipate investing in the stock market. The millennials also want to invest more in education and development of their skills, which will surely give a boost to the education sector.

In the advertising world, print and outdoor media have taken a major hit as people during the lockdown had little option but to move to digital news portals and OTT platforms. Most of the population is binge watching on all the major OTT platforms. Video calling apps have also gained great popularity thanks to official meetings and social hangouts being restricted to our laptop/mobile screen. Will these trends stay after the lockdown ends? On that note, 36 per cent of the respondents said that their online shopping will increase, and whopping 86 per cent say that they will notice OOH advertising as much or more than they did before!

References from the reports by The Reserve Bank of India, The International Monetary Fund and McKinsey and Company were also taken into account while making the report.

Laqshya Media Group CEO Atul Shrivastava believes that people in India are committed to fight and win over the current situation. He said, “There is a huge consumption of every product in India and there will be eagerness amongst the brands to become the first choice for every consumer. This is likely to fuel the demand for the advertising sooner than most nay-sayers predict.”

Laqshya Media Group MD Alok Jalan is positive of the way ahead, “Although some industries have taken a major hit, others like the e-commerce businesses have a lot of scope ahead. This is also a good opportunity for the traditional businesses to evolve their digital presence. If we are able to contain the pandemic shortly then there is a scope for the market to bounce back and show growth.”

Follow Tellychakkar for the consumer facing news & entertainment

MAM

Lego brings Messi, Ronaldo, Mbappé, Vinicius together

Campaign clocks 314 million views ahead of FIFA World Cup 2026 buzz.

MUMBAI: Four legends, one frame and not a single tackle in sight. Lego has pulled off a crossover few thought possible, uniting Lionel Messi, Cristiano Ronaldo, Kylian Mbappé and Vinícius Júnior in a single campaign ahead of the FIFA World Cup 2026 only this time, they’re building dreams brick by brick.

Titled “Everyone wants a piece”, the campaign features the quartet assembling a Lego version of the World Cup trophy, before placing miniature versions of themselves atop it, a playful nod to football’s ultimate prize. Shared widely across social media, the ad carries a pointed disclaimer: it is not AI-generated, a subtle but telling signal in an era where even reality is often questioned.

The numbers tell their own story. The campaign has already crossed 314 million views on Instagram across the players’ accounts, with fans hailing it as a rare, almost nostalgic moment particularly for the reunion of Messi and Ronaldo, whose last shared campaign ahead of the 2022 World Cup became one of the platform’s most-liked posts.

Beyond the film, Lego is extending the play with exclusive, player-themed sets tied to each of the four stars, part of a broader football-led programme designed to ride the global momentum building towards 2026. The idea, as echoed by the players themselves, leans into the parallels between football and play experimentation, creativity, failure, and triumph.

Messi described the sets as a way to bring on-pitch moments into an imaginative, hands-on world, while Ronaldo called the transformation into a Lego figure a rare honour, blending sport with storytelling. Vinícius, meanwhile, struck a more personal note, recalling childhood moments of building with Lego and framing creativity as a universal language that transcends borders.

The timing is no accident. With the 2026 World Cup set to run from June 11 to July 19 across the United States, Canada and Mexico, and featuring an expanded 48-team format, global anticipation is already building. Argentina, led by Messi, will enter as defending champions, adding another layer of intrigue.

For Lego, the campaign does more than celebrate football, it taps into its mythology. Because when icons become figurines and rivalries turn into play, the beautiful game finds a new kind of pitch. one built, quite literally, by hand.