Brands

Factories feel the heat but keep rolling in Q3 FY26

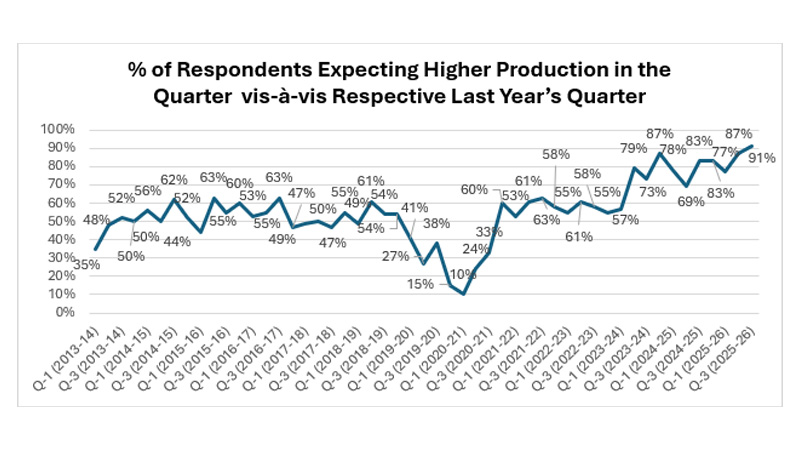

MUMBAI: When factory floors hum, the economy listens and India’s manufacturing units are still making noise. The latest FICCI Quarterly Survey on Manufacturing paints a picture of steady momentum in Q3 FY25–26, with confidence holding firm even as costs stay stubbornly high.

Covering eight major sectors and manufacturers with a combined turnover of over Rs 3 lakh crore, the survey finds that around 91 per cent of respondents reported higher or unchanged production in Q3, up from 87 per cent in the previous quarter. Domestic demand also stayed resilient, with 86 per cent expecting order books to be higher or stable, aided in part by recent GST rate cuts.

Capacity utilisation across manufacturing hovered at a healthy 75 per cent, signalling sustained economic activity. Metals and metal products led the pack at 79 per cent, followed closely by electronics and electricals at 78 per cent, while auto components operated at a more measured 65 per cent. Investment intentions over the next six months remained steady, though global uncertainty, geopolitics and regulatory challenges continued to temper expansion plans.

Exports offered cautious cheer. More than 70 per cent of respondents expect overseas shipments in Q3 to be higher or unchanged compared to a year ago, while inventories largely stayed in check, with 83 per cent anticipating stable or higher stock levels.

The pressure point remains costs. Nearly 57 per cent of manufacturers reported an increase in production costs as a share of sales, driven by higher raw material prices, currency depreciation, logistics expenses and power tariffs. Despite this, access to finance remained supportive, with over 87 per cent reporting adequate availability of funds and average interest rates hovering around 8.9 per cent.

On the jobs front, the mood was measured but positive. Thirty-eight per cent of respondents plan to add workers over the next three months, up from 35 per cent a year ago, even as concerns over skilled labour availability persist in select sectors.

Sectorally, electronics and electricals stood out with strong growth expectations, while most others from capital goods to textiles and auto components are bracing for moderate expansion in the 5–10 per cent range. The message from factory gates is clear: growth is holding its ground, but the path ahead calls for policy support, cost relief and sharper competitiveness to keep the wheels turning.