Brands

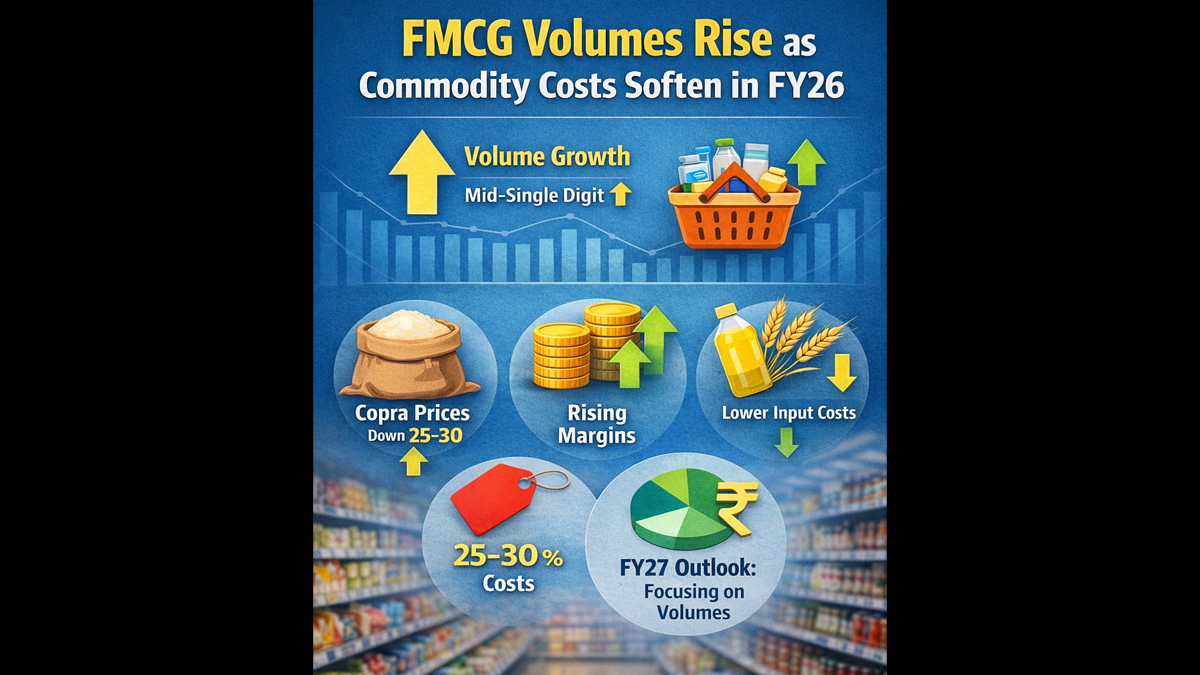

After price hikes, FMCG bets on volume growth in FY27

Easing input costs and firmer rural demand set the stage for fatter margins in FY27

MUMBAI: India’s consumer giants are shifting gears. After a year of price-led gains, fast-moving consumer goods makers are betting that FY27 will belong to volumes.

With inflation ebbing and commodity costs softening, sector leaders expect growth to be driven less by price hikes and more by shoppers returning to baskets. In the December quarter, most large FMCG firms clocked mid- to high single-digit volume growth, signalling that demand is stirring after bouts of volatility.

Key inputs are turning benign. Edible oils, wheat, copra and surfactants have softened. Coconut oil and SLES prices are easing. Vegetable oil costs have cooled. Wheat flour dipped marginally in the third quarter of FY26. Copra prices, which had spiked abnormally, have corrected by 25 to 30 per cent. With GST rationalisation, higher MSPs and a healthy crop season lending macro tailwinds, companies see a constructive backdrop for both urban and rural markets.

Price hikes have largely been taken earlier in the fiscal year. Now the playbook is different. Companies are weighing selective consumer offers, higher grammage and calibrated discounts to pass on some of the input cost relief, even as they remain watchful of rollover impacts from past increases.

Rural India continues to outpace cities. Urban demand has improved sequentially, but the countryside remains the steadier engine of growth.

At Dabur India, Mohit Malhotra, chief executive, sees next year’s expansion tilting decisively towards volume rather than pricing, though residual price effects from September hikes may linger.

Marico is banking on moderating inflation and improved affordability to drive a gradual recovery in consumption. Saugata Gupta, managing director and chief executive, expects operating profit growth to strengthen as input pressures subside. The maker of Saffola, Parachute and Livon aims to sustain volume momentum even as pricing growth moderates.

At Britannia Industries, margins are described as healthy, supported by stable commodity prices. Rakshit hargave, managing director and chief executive, points to wheat trends and seasonal dynamics in February and March as crucial indicators, but sees stability for now.

Hindustan Unilever reports a steady improvement in the operating environment and underlying demand. Priya Nair, chief executive and managing director, flags rising consumer confidence, backed by the RBI’s consumer survey, as a sign that willingness to spend is reviving. Niranjan gupta, chief financial officer, expects FY27 to outpace FY26 on the back of sustained recovery.

Godrej Consumer Products remains confident of high single-digit consolidated revenue growth. Sudhir Sitapati, managing director and chief executive, expects the India business to deliver continued growth while maintaining normative EBITDA margins. Internationally, the GAUM cluster spanning Africa, the United States and the Middle East is tipped to post double-digit revenue and profit growth, even as temporary macro and pricing pressures in Indonesia and Latin America weigh on full-year EBITDA expansion. The company expects a robust exit trajectory into FY27, with momentum carrying through the fourth quarter of FY26.

The direction of travel is clear. With costs cooling, confidence firming and rural demand holding steady, India’s consumer heavyweights are done leaning on price tags. The next leg will be fought on volumes, velocity and who can fill more baskets, faster.

Note: Certain inputs are based on reporting by The Economic Times.

Brands

Dunkin’ Donuts to exit India as Jubilant FoodWorks ends 15-year franchise deal

The quick service restaurant giant is ending a 15-year franchise partnership with the American doughnut chain, even as it renews its Domino’s agreement for another 15 years

NOIDA: Dunkin’ is done in India. Jubilant FoodWorks Ltd, the country’s leading quick service restaurant operator, has decided not to renew its franchise agreement with the American coffee and doughnut chain, and will wind down its Indian stores in a phased manner before December 31, 2026, bringing a 15-year partnership to a quiet, loss-laden close.

The decision, approved by JFL’s board on March 30, 2026, ends a relationship that began with a Multiple Unit Development Franchise Agreement signed on February 24, 2011. JFL will now evaluate and undertake what it described in a regulatory filing as the “rationalisation and/or cessation of certain operations and/or sale, transfer or disposal of assets and/or assignment or transfer of franchise rights,” all in consultation with Dunkin’s brand owners and strictly within the terms of the original agreement.

The numbers tell the story bluntly. In the financial year 2024-25, Dunkin’ India posted a revenue of Rs 37 crore against a loss of Rs 19 crore — a haemorrhage that was always going to test the patience of a parent company recording revenues of Rs 6,104 crore and a profit of Rs 194 crore in the same period. Doughnuts, it turns out, were never going to move the needle.

The contrast with JFL’s handling of its other marquee franchise could hardly be sharper. Even as it walks away from Dunkin’, the company has just doubled down on Domino’s, signing a fresh Master Franchise Agreement on March 31, 2026, granting it exclusive rights to develop and operate Domino’s Pizza stores in India for 15 years, with an option to renew for a further 10.

JFL, incorporated in 1995 and promoted by the Bharatia family, operates a network of more than 3,500 stores across six markets — India, Turkey, Bangladesh, Sri Lanka, Azerbaijan and Georgia. Its portfolio includes Domino’s and Popeyes on the global side, and two home-grown brands: Hong’s Kitchen and COFFY, a café brand in Turkey.

For Dunkin’, India was always a stretch. The brand never quite cracked the cultural code in a market where filter coffee and chai command fierce loyalty and where the doughnut remains, at best, an occasional indulgence rather than a daily habit. Fifteen years, mounting losses and a parent with better things to spend its capital on was always going to be a difficult equation to solve.

The doughnut has had its last day. The pizza, however, is staying.