MAM

RentoMojo launches video emphasizing the concept of subscription

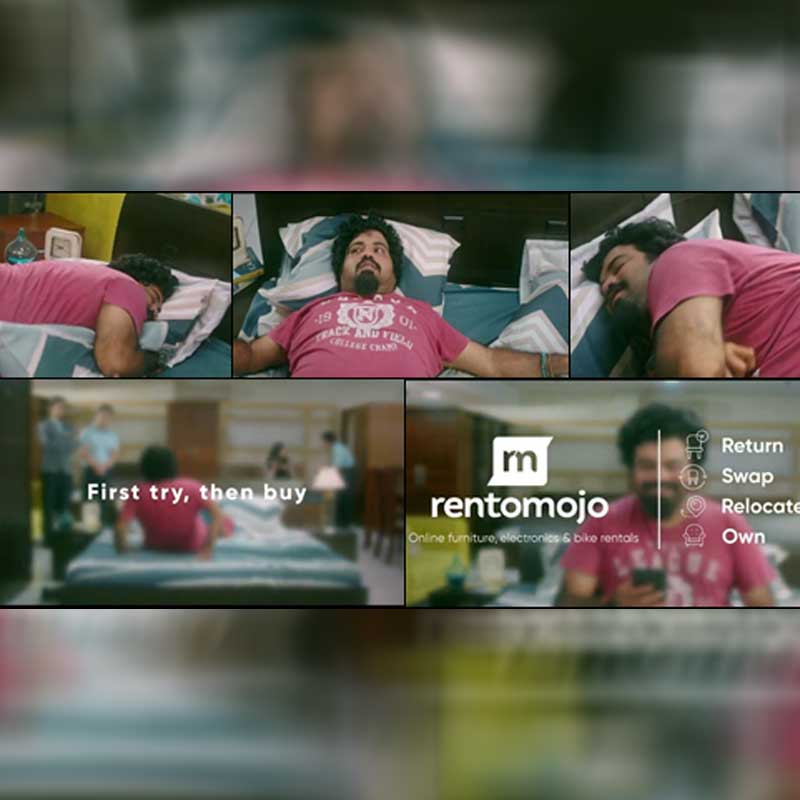

MUMBAI: RentoMojo, a pioneer in lifestyle subscription & consumer leasing business, announces the launch of its online video highlighting the benefits of the unique propositions of ‘rent to own,’ of assets procured from the company through subscription – Rental Monthly Instalments (RMI).

The video primarily targets a generation that is constantly on-the-move, while also dreading the prospect or the hassles associated with relocation such as shipping large household assets like furniture and appliances.

While ownership of such assets through outright purchase puts the onus of transportation and installation on the buyer, subscription of these from RentoMojo relieves the subscriber of these worries, thereby making it an extremely practical and effortless option. It also targets consumers who are wary of investing large sums in household assets, doubtful of its utility, comfort or longevity.

RentoMojo has launched this video as a part of their campaign that uses relatable life scenarios, combining them with light humour and metaphor to distinguish the brand’s unique propositions and to enhance its recall value. The narrative is short and to the point, yet highly effective, as it is aligned with some of the key consumer pinpoints.