iWorld

AT&T-DirecTV deal draws mixed reactions from media analysts, shareholders

NEW DELHI: The recent announcement about American telecom carrier AT&T making a $48.5 billion bid for DirecTV has led to heated debate both in the media in the United States as well as among shareholders, stock watchers and industry stakeholders.

Some analysts are questioning if the deal is so fruitful then why companies like Apple, Verizon and Google never considered purchasing DirecTV.

According to various reports in the media in the US, DirecTV shareholders are reportedly happy with the price and shareholder rights attorneys at Robbins Arroyo are investigating the proposed acquisition.

DirecTV shareholders will receive $28.50 in cash and $66.50 in shares of AT&T stock for each share of common stock, for a total consideration of $95.

Robbins Arroyo’s investigation focuses on whether the board of directors at DirecTV is undertaking a fair process to obtain maximum value and adequately compensate DirecTV shareholders, who were expecting more.

The $95 merger consideration is significantly below the target price set by at least four analysts, including a target price of $100 set by analysts at Macquarie Group and Atlantic Equities. The company’s comparable adjusted earnings per share beat analyst estimates in three out of its last four quarters, said Robbins Arroyo.

DirecTV shareholders have the option to file a class action lawsuit to ensure the board of directors obtains the best possible price for shareholders and the disclosure of material information.

AT&T has also been under attack from Fitch Ratings that has placed the ‘A’ Issuer Default Ratings (IDRs) and outstanding debt of AT&T and its subsidiaries on Rating Watch Negative. The company’s ‘F1’ short-term IDR and commercial paper rating has also been placed on Rating Watch Negative.

Meanwhile, Fitch has placed the ‘BBB-’ IDR and outstanding debt ratings assigned to DirecTV Holdings on Rating Watch Positive. Approximately $20.8 billion of debt outstanding at DirecTV as of 31 March 2014 is affected by Fitch’s action.

Fitch said AT&T’s acquisition of DirecTV will improve its financial flexibility owing to DirecTV’s strong free cash flows and the significant equity component in the transaction financing. The transaction also strengthens the company’s position in the video landscape, offering the potential to capitalise on trends for mobile video and over-the-top (OTT) video delivery. The acquisition also diversifies AT&T’s revenue stream.

DirecTV’s video assets are complementary to AT&T’s operations, but the longer term strategic benefits are less clear and depend on the post-merger company’s ability to capitalise on emerging trends in the industry, Fitch said.

But AT&T’s planned acquisition of DirecTV offers benefits in the form of a nationwide footprint for AT&T as a video over the top (OTT) and pay TV operator and ties in with the company’s already strong IPTV, broadband and wireless businesses, said Strategy Analytics.

“The industry is at a turning point where fixed operators are under tremendous pressure from increasing costs but DirecTV is known for having a higher-end customer base, and the ARPU for the company reflects the premium service,” said Strategy Analytics service provider strategies director Jason Blackwell.

Multi-play bundling is an important strategy for AT&T, indicated by the high number of its customers who subscribe to three and four services. Targeting high ARPU, premium customers with DirecTV plays well into AT&T’s strategy. Through this deal, AT&T is buying scale in Pay TV, premium customers for greater multi-play service adoption, and a nationwide footprint for quad-play services.

AT&T will probably be able to integrate DirecTV spectrum and delivery mechanisms as well as OTT Video services even more rapidly if the new FCC Net Neutrality rules are adopted. “It looks as if AT&T has placed a major bet on this happening. These FCC rules could dramatically simplify the delivery of multi-device multi-service ‘multiplay’ bundles across fixed and wireless; and even stimulate innovation in fixed telco services based on mobile features,” said Sue Rudd, director, Service Provider Analysis for Wireless Networks and Platforms.

America Movil has no plans to buy any significant portion of AT&T’s stake, according to a report from Bloomberg. A public sale of AT&T’s 8 percent holding is seen as the most likely scenario. Such a secondary offering could let America Movil owner Carlos Slim and his family add to their personal stakes if they choose.

Fortune reported that AT&T’s $49 billion agreement to buy DirecTV is a promise to build and enhance high-speed broadband for 15 million U.S. customers, many of whom live in rural areas that can be difficult to reach at a viable cost.

The $48.5 billion deal could fall apart if the satellite-TV company is unable to renew its NFL Sunday Ticket service, a premium package offering access to all out-of-market games for $39 per month.

Football could play a decisive role in the megamerger. The breakup provisions stipulate that AT&T would be able to litigate and potentially collect damages if DirecTV fails to use “it’s reasonable best efforts to obtain such a renewal” of NFL Sunday Ticket, according to a filing with the Securities and Exchange Commission, said a Business Week report.

Meanwhile, Infonetics Research has reduced its 2017 pay-TV revenue forecast by 35 per cent globally, from $401 billion to just under $260 billion. It said the overall video services ARPU and revenue growth will be constrained.

“This is because of the result of increasing competition from OTT (over-the-top) players and the service providers themselves using broadband video as a lower-priced offering,” said Jeff Heynen, principal analyst for broadband access and pay TV at Infonetics Research.

Gaming

India’s broadcasters say no to Fifa World Cup 2026

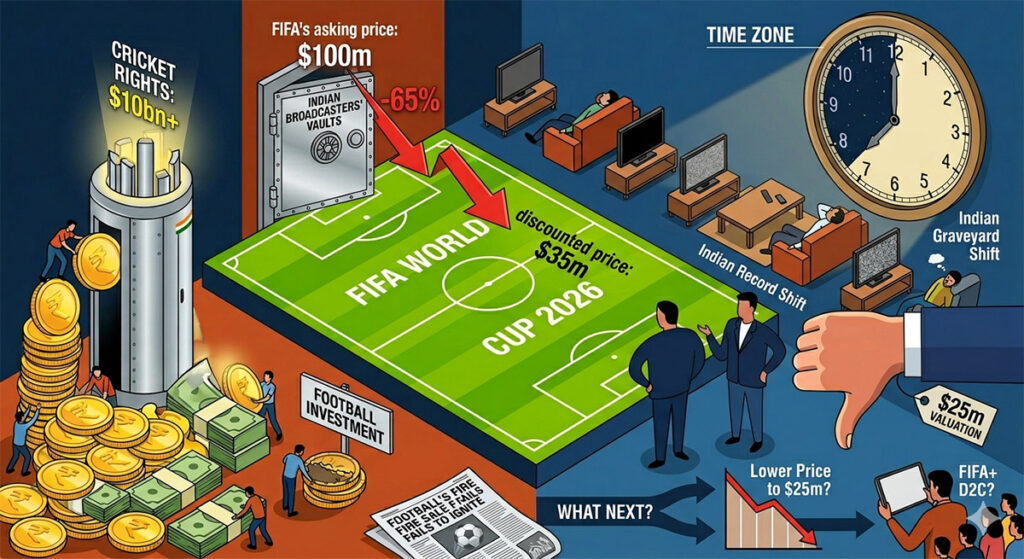

Fifa has slashed its asking price by 65 per cent but India’s broadcasters are still not buying

MUMBAI: The world’s biggest sporting event cannot find a single taker in the world’s most sports-mad nation. Fifa’s television rights for the 2026 World Cup remain unsold in India, and the clock is ticking loudly.

To shift the property, world football’s governing body has already swallowed hard and cut its asking price from $100m to $35m, bundling in the 2030 edition as a sweetener. It has not worked. Indian broadcasters have looked at the offer, done the sums and quietly walked away.

The reasons are brutally simple. The 2026 tournament, co-hosted by the United States, Canada and Mexico, kicks off in a time zone that turns India’s primetime into a graveyard shift. Most matches will air between midnight and 7am IST, a scheduling catastrophe for advertisers chasing mass reach. The 2022 Qatar edition was a gift by comparison, with matches dropping neatly into Indian evenings. North America offers no such luxury.

The market itself has also changed beyond recognition. The merger of Star India and Viacom18 into JioStar has gutted the competitive tension that once sent sports rights prices soaring. Where rival bidders once slugged it out, there is now a single dominant buyer, and it is in no hurry. JioStar has valued the rights at roughly $25m, a full $10m below Fifa’s already-discounted floor price. That gap has so far proved unbridgeable.

Broadcasters are also nursing a ferocious cricket hangover. Between 2022 and 2023, Indian media houses committed well over $10bn to cricket rights alone, covering IPL, ICC events and BCCI domestic fixtures combined. After a binge of that scale, appetite for a football package that delivers a fraction of the ratings, in the dead of night, is close to zero.

The economics of football broadcasting make the maths even harder. Cricket, with its natural breaks every few overs, is an advertiser’s paradise. Football offers a 15-minute halftime and precious little else. Recovering a nine-figure rights fee from a single half-hour ad window is a stretch at the best of times. These are not the best of times: the Indian government’s tightening grip on real-money gaming and gambling advertising has vaporised a category that once underwrote the economics of big sporting events.

Nor is the World Cup an anomaly. Indian Super League valuations have cratered. English Premier League rights have softened across successive cycles. The cooling of football as a broadcast commodity in India is structural, not cyclical.

With the tournament opening on 11th June, Fifa is running out of road. It may yet blink and meet JioStar at $25m. Or it may go direct, streaming the entire tournament on its own platform, Fifa+, or cutting a digital deal with YouTube, and hoping that a generation of Indian football fans finds its way there without a broadcaster to guide them.

Either way, the beautiful game’s Indian chapter is looking decidedly ugly.