MAM

India’s taxi war may be headed for a truce

MUMBAI: Gone are the days when we had to book a cab by calling a local can agency, and that’s because cab aggregators in India have completely changed the way we book a cab.

Back in the day, while Mumbai had its distinguished kaali-peelis, Delhi had its metro whereas Bengaluru didn’t have a great public transport system. Cabs were never a mode of transport in India until a few years ago.

India’s first official cab service began in Mumbai in 2007 with Meru cabs, who were extremely high priced but came in handy during airport and long-distance travels. It was in 2011, when cab service provider TaxiForSure eased the booking process by starting an online portal, aggregating multiple cab agencies. They grew in popularity by including an Android-based GPS system, which helped customers track their ride.

Meanwhile, Ola, which started in 2010, was following a different model by associating directly with cab drivers, thereby eliminating the need for cab agencies. The company gained popularity only in 2013 as in the initial years, people couldn’t relate with the idea of talking to the driver directly on booking a cab and questioned the model’s authenticity. It was around the same time that global taxi market leader Uber entered the Indian market but failed to connect with the audience as it only allowed credit cards as a mode of payment.

Over the years, a lot has changed in the Indian cab aggregator sector, where some had to shut shop or were bought over due to bankruptcy and increasing losses. In March 2015, OlaCabs acquired TaxiForSure for approximately US $200 million and Geotagg, a trip-planning applications company, for an undisclosed sum. The company also acquired Foodpanda’s business in India in 2017.

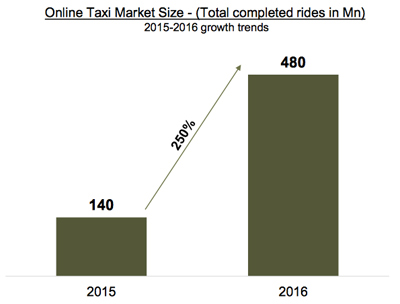

The segment has gained a lot of attention due to huge funding, highly competitive pricing (Ola-Uber on-going price war), security issues of women passengers and tussle with the government for license and permits.

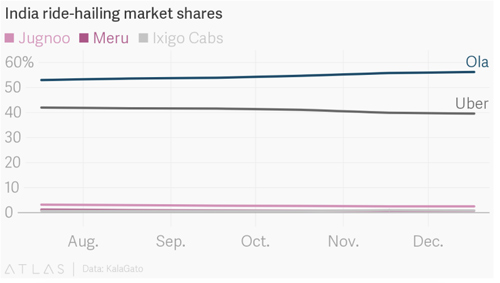

Today, Ola clocks an average of more than 150,000 bookings per day and commands 60 per cent of the market share in India, while Uber’s shares have slipped from 42 per cent in July 2017 to 40 per cent in December 2017. According to Japanese multinational conglomerate, SoftBank, the organised taxi sector in India may be worth $7 billion by 2020.

In 2016, Uber made a deal with its Chinese rival Didi Chuxing to exit the Chinese market, after the duo fought hard for the country’s huge customer base Uber also exited Russia and Eastern European markets last year after reaching a similar deal with Yandex, giving Uber 36.6 percent of the entity formed by the two companies.

SoftBank has made major investment in Ola and Uber who has also invested in Grab, which is Uber’s rival in South East Asian countries. Ever since Uber inked the deal with SoftBank, there have been speculations that Uber would pull out of those markets and it turned into a reality earlier this year where Uber sold its business in SEA to Grab.

Now, news is doing the rounds in market that a possible merger between Ola and Uber may be on its way in India. Since the Ola-TaxiForSure acquisition, the Indian market has essentially been a two-horse race and now, were the Uber-Ola deal to work out, we'd witness a monopoly situation like never before as Uber and Ola, together hold nearly 95 per cent of the market today.

If the merger does happen, we may see increase in advertising and marketing for the new merged entity as Ola and Uber are India’s two major cab aggregators with pockets filled. Ola has a robust advertising budget for television and print whereas Uber has an upper hand at digital and social media marketing. The combined entity would indicate 360-degree advertising including print, out of home, television and digital.

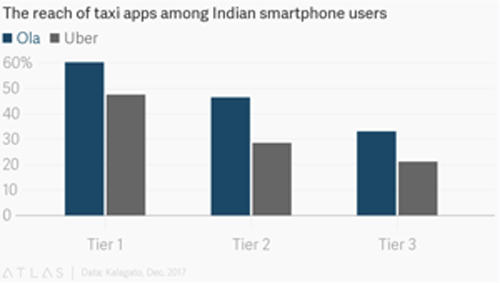

While Uber has always had an elite and urban vibe to it, Ola has a stronger presence across smaller towns and segments. The Indian firm operates in 110 cities, far more than Uber’s 31. The merged entity would ensure a better penetration in rural as well as urban markets as the customer base for both the apps would be aligned together.

This would also mean the prices would be kept in check as currently, Ola is assumed to be comparatively cheaper and affordable than Uber. But this could also go the other way, as a monopoly could lead to price tampering and exorbitant charges.

But the merger will also open the field for newer players to enter in the segment which will only help in competitive prices and all of them striving to serve better in order to acquire and retain customers.

All said and done, when and how the merger will unfold is a story for another day but if there’s one thing, it will definitely be an interesting tale to tell.

Also Read :

2018 will be a year of video campaigns: WATConsult's Rajiv Dhingra

Competing with consumer activities not brands: Kingfisher's Sheikhawat

Cinema advertising begins to take centre stage

Gold has evolved from a traditional family heritage to one of the most effective instruments for high-speed liquidity in the rapidly changing financial world of 2026. With 22K gold prices remaining stable at ₹14,440 per gram and 24K gold hitting ₹15,752 per gram as of February 21, 2026, the Indian gold market is seeing a historic increase. A rather small quantity of jewels can now unleash significant cash due to their increased worth.

Finding the best gold loan, however, takes more than simply visiting the closest branch because there are several banks and NBFCs (Non-Banking Financial Companies) vying for your business. It necessitates a strategic grasp of how lenders set their product prices. The cost of borrowing in 2026 is no longer a “one-size-fits-all” number; rather, it is a variable that depends on your loan amount, the state of the market, and particular regulation slabs. You may make sure that you leverage your gold holdings at the best gold loan interest rates by taking a methodical approach.

Recognise the Tiered LTV Framework for 2026

The Reserve Bank of India’s (RBI) introduction of tiered Loan-to-Value (LTV) criteria is one of the biggest changes. Depending on your unique financial needs, this policy directly affects which lender can provide you with the best gold loan.

The LTV limitations for 2026 are set up as follows:

- Loans up to ₹2.5 Lakh: 85% LTV eligibility

- Loans up to 80% LTV are eligible for those between ₹2.5 Lakh and ₹5 Lakh

- Loans over ₹5 lakh are eligible for up to 75% LTV

You must match your borrowing with these levels to determine the lowest gold loan interest rate. Because there is less risk involved, a lender may frequently give a cheaper rate for a 75% LTV plan than for an 85% LTV plan. Choosing a lower LTV bracket is a tried-and-true method to get the finest gold loan conditions if you don’t require the highest amount of cash on hand.

Compare the Offerings of Banks and NBFCs

The best gold loan is determined by your preference for quickness or cheaper cost. The service and pricing differences between ordinary banks and specialised gold lending NBFCs have grown.

Public and Private Banks: The interest rates on gold loans offered by public and private banks are often the lowest on the market, frequently beginning as low as 8.75% to 9.50% annually. Borrowers seeking a long-term or overdraft-like facility who already have a savings account will find it appropriate.

NBFCs: They are the industry leader in offering a genuine, rapid gold loan experience, even if their interest rates may be a little higher than those of banks. They are frequently the best gold loan option for urgent needs when speed surpasses a 1% yearly cost difference, thanks to doorstep services and quick disbursals.

Make Use of Purity’s Power

The most potent “multiplier” in your loan computation is the karat of your jewellery. Lenders have shifted to highly standardised assaying procedures. Declaring high-purity materials helps you get a higher valuation and a better loan amount.

Make sure you are offering hallmarked jewels in order to receive the best gold loan. Because the collateral risk is essentially zero, hallmarked gold (BIS 916) lowers the lender’s uncertainty during appraisal and frequently enables them to provide a more alluring gold loan interest profile.

Consider the Mode of Repayment

The best gold loan is one that doesn’t negatively impact your monthly cash flow. Below are a few repayment options you may consider:

- Bullet Repayment: At the conclusion of the term, which is usually 12 months, you pay the whole amount. Although the cumulative interest cost of the gold loan may be somewhat greater, this is great for short-term liquidity.

- Monthly Interest Payment: You just pay the interest each month; the principal is paid at the end. As a result, the monthly burden is minimal.

- EMI (Principal + Interest): The most organised approach to loan closure is through EMI (principal + interest), which progressively lowers your principal and, as a result, your overall interest expense.

Use a computerised gold loan calculator to determine which option delivers the biggest savings before you sign the contract. Even a 0.5% change in the repayment schedule might save you thousands of rupees on a big loan in the expensive year of 2026.

Be Aware of Unexpected Fees and Penalties

High administrative costs can occasionally be concealed by a low headline interest rate on gold loans. Searching for the finest gold loan requires you to consider the “Total Cost of Credit.”

- Processing costs: For loans up to ₹3 lakh in 2026, several banks provide “Nil” processing costs.

- Make sure valuation fees are clear and do not represent a portion of the loan balance.

- Prepayment and Foreclosure Penalties: You shouldn’t have to pay a large penalty if you decide to end your gold loan early.

- Late Payment Fees: Examine gold loan interest “steps up” if you fail to make a payment. Some lenders charge 2% monthly punitive interest on the past-due balance, which can easily get out of hand.

Conclusion

Finding the greatest gold loan in 2026 requires striking a balance between the historic worth of your gold, i.e., ₹14,440 per gram, and a lender who understands your desire for quickness and transparency. You may make sure that your gold is a bridge to your financial objectives rather than a burden by comparing the tiered LTV brackets and selecting a repayment schedule that corresponds with your income. The knowledgeable borrower usually prevails in a market where gold loan interest rates are more competitive than ever. Spend some time evaluating at least three lenders, confirming that they are in accordance with the RBI as of 2026, and confidently discovering the actual worth of your assets.

FAQs

How much can I borrow in gold today, per gram?

The maximum credit amount for loans under ₹2.5 lakh (85% LTV) is around ₹12,274 per gram as of February 21, 2026, when 22K gold is valued at ₹14,440 per gram. Make sure your decorations are made of pure gold with minimal stone deductions to receive the greatest gold loan value.

Does my gold loan interest rate depend on my credit score?

In general, no. The majority of lenders offering a quick gold loan do not significantly rely on your CIBIL score because it is a secured loan. However, with certain private banks in 2026, having a solid credit history might help you get greater loan amounts or “preferred” gold loan interest rates.

How can I figure out how much interest is due on a gold loan?

The straightforward calculation is as follows: Principal x Annual Rate x Tenure (in years). Many lenders include a best gold loan calculator on their smartphones for a more accurate 2026 figure. This tool automatically adjusts for your selected repayment method and particular LTV tier.

In 2026, would I be able to obtain a gold loan for 18K jewellery?

Yes, most lenders accept 18K gold. However, the interest rate on the gold loan and the value per gram will be different because the purity is 75% as opposed to 91.6% for 22K. Before using the current market cost of ₹14,440 per gram, lenders first convert your 18K weight into a 22K equivalent.

If I close my gold loan early, will I be penalised?

Prepayment penalties are not imposed by the majority of respectable lenders providing the best gold loan in 2026. However, if you end the loan nearly immediately after disbursement, some may demand a minimum interest payment of seven to fifteen days. Verify your agreement’s “Foreclosure” clause at all times.