Software

Visa-OpenAI shopping partnership raises questions over whether convenience is worth the risk

As agentic commerce shifts from consumer retail to automated B2B procurement, the financial sector faces an untested regulatory frontier where algorithms hold the wallet.

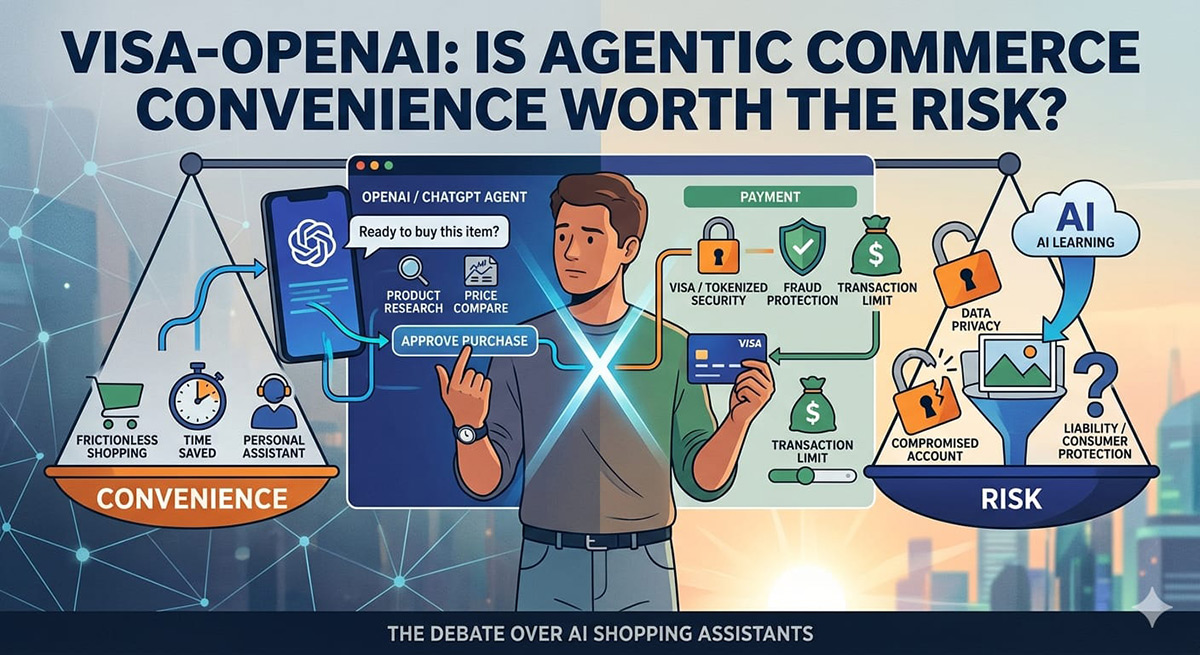

MUMBAI: Visa and OpenAI have announced a strategic partnership that will allow ChatGPT and other OpenAI-powered AI agents to complete purchases on behalf of users, marking a major step toward what the companies describe as the future of “agentic commerce”.

Under the agreement, announced at the Visa Payments Forum in San Francisco, Visa’s payment network will be integrated directly into OpenAI’s AI experiences. This enables users to search for products, compare options, and authorize purchases through conversational prompts. The system will work anywhere Visa is accepted, potentially giving AI agents access to millions of merchants worldwide.

Visa said it will provide tokenization, fraud protection, and real-time transaction authorization, while OpenAI’s technology will handle product discovery, recommendations, and purchasing decisions. Users will be able to set spending limits, approval requirements, and merchant restrictions before allowing AI agents to make transactions. The partnership forms part of Visa’s broader “Intelligent Commerce” initiative, which aims to position AI agents as active participants in digital commerce rather than simple recommendation tools.

While the announcement highlights a future of frictionless shopping, it also raises significant questions about security, privacy, and consumer control.

The Enterprise Frontier: Reimagining B2B Procurement

While early attention has focused on consumer shopping, the partnership features a significant, underreported enterprise layer. Beyond retail, Visa and OpenAI have committed to co-developing a range of business applications, specifically targeting automated corporate procurement, expense control, and policy-driven operational flows.

Central to this B2B push is the integration of OpenAI’s developer-focused ecosystem, Codex. By combining algorithmic intelligence with programmable payment parameters, companies will be able to deploy specialized software agents capable of autonomously negotiating vendor contracts, reordering company inventory, and clearing invoices.

For example, a corporate supply-chain agent could analyze inventory deficits, cross-reference pricing metrics across multiple verified suppliers, and execute high-volume card-to-account payments using secure, tokenized credentials—all within rigid internal compliance guidelines set by a human CFO. This shifts the enterprise focus away from manual data entry toward automated financial utility.

Verifying the Machine: Agent Scores and Directories

To support this massive structural migration, Visa is rolling out specialized trust infrastructure that goes beyond standard consumer data encryption. In an ecosystem where software code buys from other software code, authentication requires an entirely new framework.

Visa introduced Agent Score, a metrics system that allows businesses to evaluate whether their websites are legible and structurally ready for autonomous AI systems to navigate and buy from them. Alongside this, an Agentic Directory will serve as a cryptographic registry. Merchants will use it to verify that an incoming purchasing agent is a legitimate, authorized entity, while the AI agents themselves can use the network to confirm they are transacting with genuine, secure business channels.

The Hallucination Liability: Who Pays for an AI’s Mistake?

Despite these structural safeguards, critics argue that linking payment credentials to AI assistants increases potential exposure if user accounts are compromised. Although Visa says payment information will remain protected through tokenization and will not be directly accessible to AI systems, a ChatGPT account with spending authority could become a valuable target for cybercriminals.

There are also deep operational concerns regarding AI reliability. Large language models can misunderstand prompts, misinterpret shipping guidelines, or experience severe hallucinations. This creates a legal gray area for banking networks.If an authorized business or consumer agent buys the wrong item due to a software glitch, consumer protection laws and standard dispute-resolution frameworks remain entirely untested. The industry has yet to clearly define whether such errors fall under merchant liability, model failure, or user negligence.

Furthermore, effective AI shopping assistants require access to detailed information about spending habits, purchase history, and personal preferences. As AI becomes more capable of anticipating consumer needs, the amount of personal data required to deliver those experiences is likely to increase.

Human Persuasion vs. Algorithmic Optimization

From what we have seen, Visa currently emphasizes user approvals and spending controls. However, technology platforms have historically moved towards greater automation over time. Features that begin with manual confirmation often evolve into systems requiring less human oversight in the name of convenience.

This dynamic challenges the entire foundation of digital marketing. For decades, digital commerce has assumed a human being is browsing, evaluating brand storytelling, and clicking “buy.” In an agentic economy, brands must learn to market to algorithms that ignore emotional appeals and optimize continuously against structured parameters like metadata accuracy, delivery timelines, and transparent price APIs.

“AI will transform commerce more profoundly than the internet or mobile technology ever did,” noted Visa chief product and strategy officer Jack Forestell during the launch. “As AI agents become active participants in the economy, Visa’s focus is to ensure transactions are trusted, secure and seamless.”

OpenAI head of partnerships for commerce Marco Mahrus echoed the sentiment, stating, “By integrating with Visa Intelligent Commerce, we’re building the infrastructure for secure, transparent, and user-controlled agentic transactions.”

The partnership combines Visa’s vast payments infrastructure with OpenAI’s rapidly growing AI ecosystem, creating what could become one of the most significant developments in digital commerce. However, experts say the success of AI-powered shopping will depend less on technology and more on user trust.

For many consumers and enterprises, the ideal balance may be using AI as an assistant that researches products and prepares purchases, while leaving the final payment decision in human hands. As AI agents become increasingly capable of researching, negotiating, and buying products, the central question is no longer whether the technology works. Instead, it is whether we are ready to hand an algorithm direct control over our money.