Digital

RBI proposes Rs 25,000 compensation cap for small digital fraud losses

RBI, customer bank and beneficiary bank will share payouts

NATIONAL: The Reserve Bank of India has proposed a new compensation framework for small-value fraudulent electronic banking transactions, requiring the central bank, the customer’s bank and the beneficiary’s bank to share payouts to affected customers.

Under draft rules released on Friday, compensation will be capped at the lower of 85 per cent of the net loss amount or Rs 25,000 in cases where the gross loss from a fraudulent electronic transaction is up to Rs 50,000.

The proposal comes as regulators step up efforts to strengthen customer protection amid a rise in digital banking frauds.

RBI governor Sanjay Malhotra had indicated during last month’s monetary policy announcement that the central bank planned to introduce a compensation framework for small-value digital frauds, allowing affected customers to claim relief once during their lifetime.

According to the draft guidelines, when the loss is below Rs 29,412, compensation of 85 per cent of the loss will be paid. Of this amount, 65 per cent will be borne by the RBI, while the customer’s bank and the beneficiary bank will contribute 10 per cent each.

For losses of Rs 29,412 or more but up to Rs 50,000, the compensation will be capped at Rs 25,000. In such cases, the RBI will contribute Rs 19,118, while the customer’s bank and the beneficiary bank will each contribute Rs 2,941.

If funds are later recovered after compensation has been paid, the customer’s bank must recalculate the payout based on the revised net loss and adjust the recovered amount accordingly.

Customers will be eligible for compensation only if they report the fraudulent transaction within five calendar days of its occurrence.

Complaints must be lodged both with the bank and through the National Cyber Crime reporting portal or the National Cyber Crime helpline. Banks must also confirm that the loss is bona fide under their internal processes.

Once a complaint is received, banks must compensate the customer within five calendar days, the draft rules state.

In joint accounts, only one account holder may submit a compensation claim.

The central bank has also proposed tightening transaction alerts by mandating instant SMS notifications for all electronic banking transactions above Rs 500. For transactions of up to Rs 500, banks may decide whether to send alerts based on internal policies.

Banks will not be allowed to charge customers for SMS messages sent to meet regulatory requirements or those used for promotional, marketing or customer awareness purposes.

The draft framework also calls for stronger oversight by requiring banks to periodically report complaints related to fraudulent electronic transactions to their boards or board-level committees. These reports must detail the number and value of cases across categories including card-present transactions, card-not-present transactions, internet banking, mobile banking and ATM transactions.

The RBI has invited public comments on the draft guidelines until 6 April, 2026. The rules are expected to take effect on 1 July, 2026 once finalised.

Banking officials say the proposed sharing of compensation between the RBI, the customer’s bank and the beneficiary bank is intended to increase vigilance across the digital payments ecosystem.

Digital

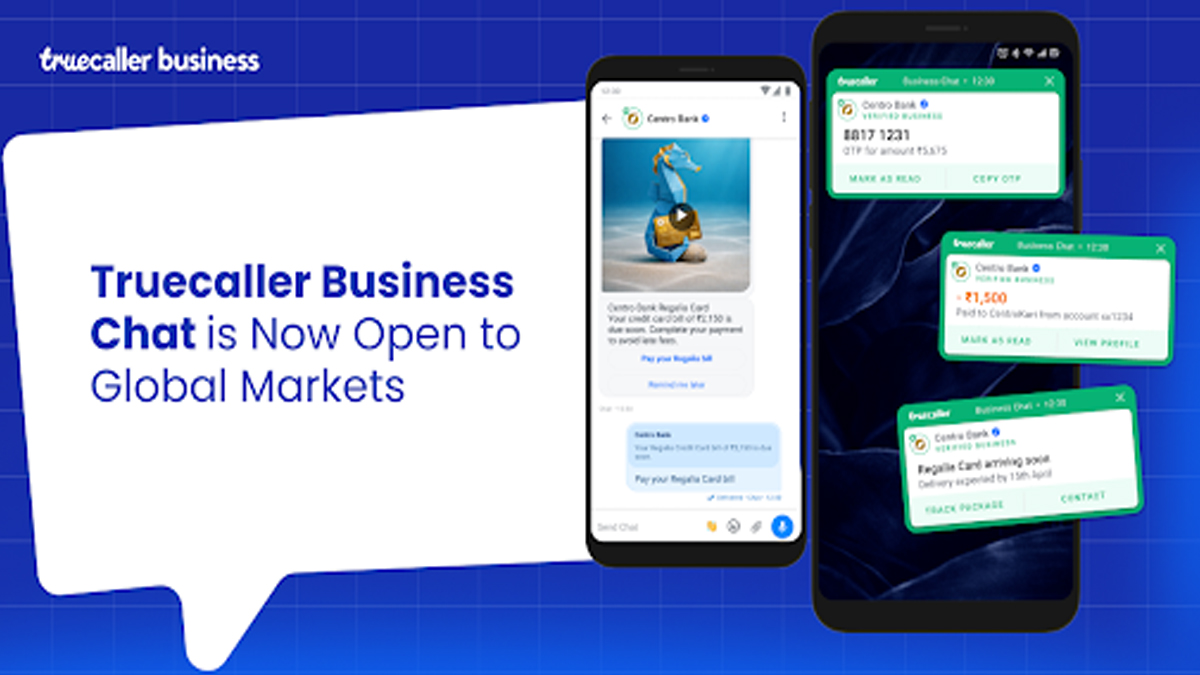

Truecaller opens Business Chat platform to global partners and enterprises

Expansion aims to replace SMS with trusted, rich and conversational messaging

MUMBAI: Truecaller has expanded access to its Business Chat platform, opening it up to global channel partners and enterprise solution providers as it looks to reshape how businesses connect with customers.

The move allows partners worldwide to offer the platform to enterprise clients, enabling a shift away from traditional SMS towards a more interactive, verified and media-rich communication experience. The company is positioning this as a higher-trust alternative in an increasingly cluttered digital landscape.

With over 500 million active users globally, Truecaller is betting on its scale and daily engagement to give brands a more direct and credible way to reach consumers. The platform supports contextual conversations, real-time insights and engagement metrics, allowing businesses to fine-tune communication across the customer journey.

“The definition of success for modern enterprises has evolved. It’s no longer just about delivery but about earning attention and driving meaningful engagement,” said Truecaller global head, GTM Priyam Bose. He added that opening the platform to partners creates a gateway for brands to connect with users in a more trusted and action-oriented environment.

The expansion is already underway, with partners such as Gupshup and OneXtel live in India, while Globe Teleservices, Cloudcom and Sling Africa are driving adoption in international markets.

By equipping partners with data-driven tools and a conversational interface, Truecaller aims to help businesses cut through noise and build stronger customer relationships. The platform also promises a cleaner, more secure interaction layer, addressing long-standing concerns around spam and trust in business messaging.

As enterprises rethink customer engagement in a post-SMS world, Truecaller’s latest push signals a clear ambition to become a central player in conversational commerce.