MAM

Digital is way forward but auxiliary for top brands: Reports (updated)

MUMBAI / BENGALURU: Two separate studies by unrelated parties have been used in this report. Mobile internet has excellent future prospects in South East Asia, and more so in India says the Indian Digital Advertising Report 2017 (DA Report) by Cheetah Global Lab.

India has, as a country, skipped right over PC and entered the mobile internet age. Although India’s mobile internet penetration remains low, the accelerated development of its infrastructure and support from local carriers have made India one of the fastest growing internet populations in the world. 4G coverage in India continues to rise, and the rural market there has considerable potential.

India differs from markets with more mature digital ecosystems, in that traditional media, especially newspapers, have not yet been seriously challenged by digital content channels. Traditional media would continue to enjoy high popularity and profit margins. Indian newspapers; revenues have continued to grow, and newspaper is still the most effective way for advertisers to reach a great number of users.

However the DA Report says that India’s digital ad market development has been hindered by insufficient infrastructure and limited internet speed, but these factors aside, digital ads are not the main advertising channel for top-tier brands. From the data it has obtained, Cheetah Lab says that it is clear that even if brands had bigger advertising budgets, Indian advertisers would retain a preference for traditional media and the non-mobile internet. According to Cheetah Global Lab, one of the main reasons for this is that at present, the Indian ad market lacks industry standard, widely accepted performance evaluation standards. Compared to digital ads, print media and television ads can provide clearer statistics for reaches and digital ad performance is harder to determine.

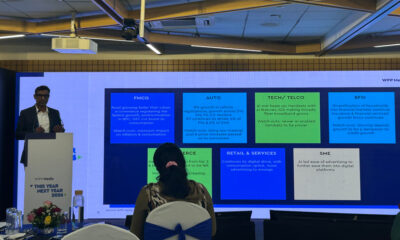

In terms of the distribution of spending on digital advertising across all vertical industries, e-commerce, accounting for 19 per cent of all digital ad spending, leads the pack. FMCG comes in second with a 14 per cent share, while banking, financial services and insurance (BFSI) follow closely behind. Consumer durables, automotive, and media & entertainment are not separated by wide margins.

When comparing vertical industries in terms of the percentage of marketing budget spent on digital advertising, e-commerce companies spend the highest percentage at 25 per cent, less than the percentage of advertising budget allocated for television advertisements (38 per cent) and print ads (28 per cent). Number two telecommunications companies allocate 22 per cent of their marketing budgets for digital advertising, followed by BFSI and media & entertainment, in which about one-fifth of advertising budgets are allocated for digital advertising. In the durable consumer goods industry, 17 per cent of advertising budgets go to digital advertising.

The major developments and conclusions of the DA Report are: In the digital age, traditional media continue to thrive in the Indian ad market; Spending on digital advertising in India will be increased in social and video; Standards for measuring ad performance, data, independent third-party verification, and visibility rates: spending on digital ads in the Indian market revolves around these keywords.

A separate report unrelated to the DA Report of Cheetah Global Labs, Indiantelevision.com found, confirms the analyses of India Mobile Video Report (a joint study by Kantar IMRB & Culture Machine) June 2017 that mobile equipment manufacturers, mobile advertisers and OTT players will be investing in mobile technologies to expand their business, explore new avenues in terms of monetisation, especially broadcasters, production units to create new content on OTT, advertisers who are ready to spend on mobile ad placements as they are exploring new opportunities in mobile marketing, where there is a surge in data traffic and addition to mobile video consumers which will open up to new avenues for digital companies.

The Mobile Video Report says further that mobile is the future as most of the data is processed through the small handheld device. Video has adopted a dual role, becoming a means of consumption and expression. There has been a rapid evolution in the way the consumer is expressing her/ his opinion. Hence the brand marketers and digital advertisers are facing distraction as there is an oversupply in data which is confusing them and depriving them from making new opportunities.

But video is future of the content marketing. The Mobile Video Report says that, mobile screen will be attracting more engagement than any other media, likely to be 37 percent higher than TV. Not only are more people turning to the mobile for entertainment, they are also watching and engaging more deeply online.

The report unfolds that daily engagement time on mobile hovers around the four-hour mark, as per the report, it has estimated that the average time of the consumer spent on entertainment is 23 per cent in the last 9 months. And it will register a hike in data traffic from 1.4 GB in 2015 to 7 GB in 2021, which is measured in data traffic per active Smartphone.

The market will grow from Rs 1,700 million in 2016 to Rs 12,300 million in 2020. The digital video subscription market is estimated to cross 12,000 million by 2020. The OTT (over the top content) is growing rapidly; already 3 out of 10 users are across on OTT video platform.

The Mobile Video Report also suggests that 65 per cent of the video surfers on the mobile belong to non-metro towns. And while most of the users are likely to be women accounting for 30 per cent to be avid consumers of mobile video.

While the report also indicates that most of the users spend 3 hours/ week on consuming mobile video, while 90 per cent of this is spent on. It means that the 2 platforms are popular with the consumers that are YouTube and Facebook.

The other indications are, that the medium is popular across the age groups, not just the young, and over half the viewers are above the age group of 25 years. In fact India has more than 20 million avid video consumers who spend more than 22 hours a month consuming video. Mobile video consumption is not just for affluent homes, more than 40 per cent of viewers belongs to SEC C/D/E homes.

Gold has evolved from a traditional family heritage to one of the most effective instruments for high-speed liquidity in the rapidly changing financial world of 2026. With 22K gold prices remaining stable at ₹14,440 per gram and 24K gold hitting ₹15,752 per gram as of February 21, 2026, the Indian gold market is seeing a historic increase. A rather small quantity of jewels can now unleash significant cash due to their increased worth.

Finding the best gold loan, however, takes more than simply visiting the closest branch because there are several banks and NBFCs (Non-Banking Financial Companies) vying for your business. It necessitates a strategic grasp of how lenders set their product prices. The cost of borrowing in 2026 is no longer a “one-size-fits-all” number; rather, it is a variable that depends on your loan amount, the state of the market, and particular regulation slabs. You may make sure that you leverage your gold holdings at the best gold loan interest rates by taking a methodical approach.

Recognise the Tiered LTV Framework for 2026

The Reserve Bank of India’s (RBI) introduction of tiered Loan-to-Value (LTV) criteria is one of the biggest changes. Depending on your unique financial needs, this policy directly affects which lender can provide you with the best gold loan.

The LTV limitations for 2026 are set up as follows:

- Loans up to ₹2.5 Lakh: 85% LTV eligibility

- Loans up to 80% LTV are eligible for those between ₹2.5 Lakh and ₹5 Lakh

- Loans over ₹5 lakh are eligible for up to 75% LTV

You must match your borrowing with these levels to determine the lowest gold loan interest rate. Because there is less risk involved, a lender may frequently give a cheaper rate for a 75% LTV plan than for an 85% LTV plan. Choosing a lower LTV bracket is a tried-and-true method to get the finest gold loan conditions if you don’t require the highest amount of cash on hand.

Compare the Offerings of Banks and NBFCs

The best gold loan is determined by your preference for quickness or cheaper cost. The service and pricing differences between ordinary banks and specialised gold lending NBFCs have grown.

Public and Private Banks: The interest rates on gold loans offered by public and private banks are often the lowest on the market, frequently beginning as low as 8.75% to 9.50% annually. Borrowers seeking a long-term or overdraft-like facility who already have a savings account will find it appropriate.

NBFCs: They are the industry leader in offering a genuine, rapid gold loan experience, even if their interest rates may be a little higher than those of banks. They are frequently the best gold loan option for urgent needs when speed surpasses a 1% yearly cost difference, thanks to doorstep services and quick disbursals.

Make Use of Purity’s Power

The most potent “multiplier” in your loan computation is the karat of your jewellery. Lenders have shifted to highly standardised assaying procedures. Declaring high-purity materials helps you get a higher valuation and a better loan amount.

Make sure you are offering hallmarked jewels in order to receive the best gold loan. Because the collateral risk is essentially zero, hallmarked gold (BIS 916) lowers the lender’s uncertainty during appraisal and frequently enables them to provide a more alluring gold loan interest profile.

Consider the Mode of Repayment

The best gold loan is one that doesn’t negatively impact your monthly cash flow. Below are a few repayment options you may consider:

- Bullet Repayment: At the conclusion of the term, which is usually 12 months, you pay the whole amount. Although the cumulative interest cost of the gold loan may be somewhat greater, this is great for short-term liquidity.

- Monthly Interest Payment: You just pay the interest each month; the principal is paid at the end. As a result, the monthly burden is minimal.

- EMI (Principal + Interest): The most organised approach to loan closure is through EMI (principal + interest), which progressively lowers your principal and, as a result, your overall interest expense.

Use a computerised gold loan calculator to determine which option delivers the biggest savings before you sign the contract. Even a 0.5% change in the repayment schedule might save you thousands of rupees on a big loan in the expensive year of 2026.

Be Aware of Unexpected Fees and Penalties

High administrative costs can occasionally be concealed by a low headline interest rate on gold loans. Searching for the finest gold loan requires you to consider the “Total Cost of Credit.”

- Processing costs: For loans up to ₹3 lakh in 2026, several banks provide “Nil” processing costs.

- Make sure valuation fees are clear and do not represent a portion of the loan balance.

- Prepayment and Foreclosure Penalties: You shouldn’t have to pay a large penalty if you decide to end your gold loan early.

- Late Payment Fees: Examine gold loan interest “steps up” if you fail to make a payment. Some lenders charge 2% monthly punitive interest on the past-due balance, which can easily get out of hand.

Conclusion

Finding the greatest gold loan in 2026 requires striking a balance between the historic worth of your gold, i.e., ₹14,440 per gram, and a lender who understands your desire for quickness and transparency. You may make sure that your gold is a bridge to your financial objectives rather than a burden by comparing the tiered LTV brackets and selecting a repayment schedule that corresponds with your income. The knowledgeable borrower usually prevails in a market where gold loan interest rates are more competitive than ever. Spend some time evaluating at least three lenders, confirming that they are in accordance with the RBI as of 2026, and confidently discovering the actual worth of your assets.

FAQs

How much can I borrow in gold today, per gram?

The maximum credit amount for loans under ₹2.5 lakh (85% LTV) is around ₹12,274 per gram as of February 21, 2026, when 22K gold is valued at ₹14,440 per gram. Make sure your decorations are made of pure gold with minimal stone deductions to receive the greatest gold loan value.

Does my gold loan interest rate depend on my credit score?

In general, no. The majority of lenders offering a quick gold loan do not significantly rely on your CIBIL score because it is a secured loan. However, with certain private banks in 2026, having a solid credit history might help you get greater loan amounts or “preferred” gold loan interest rates.

How can I figure out how much interest is due on a gold loan?

The straightforward calculation is as follows: Principal x Annual Rate x Tenure (in years). Many lenders include a best gold loan calculator on their smartphones for a more accurate 2026 figure. This tool automatically adjusts for your selected repayment method and particular LTV tier.

In 2026, would I be able to obtain a gold loan for 18K jewellery?

Yes, most lenders accept 18K gold. However, the interest rate on the gold loan and the value per gram will be different because the purity is 75% as opposed to 91.6% for 22K. Before using the current market cost of ₹14,440 per gram, lenders first convert your 18K weight into a 22K equivalent.

If I close my gold loan early, will I be penalised?

Prepayment penalties are not imposed by the majority of respectable lenders providing the best gold loan in 2026. However, if you end the loan nearly immediately after disbursement, some may demand a minimum interest payment of seven to fifteen days. Verify your agreement’s “Foreclosure” clause at all times.