Digital

44 per cent view TV News Channels as Most Trusted Source for Latest Updates – Axis My India July CSI Survey

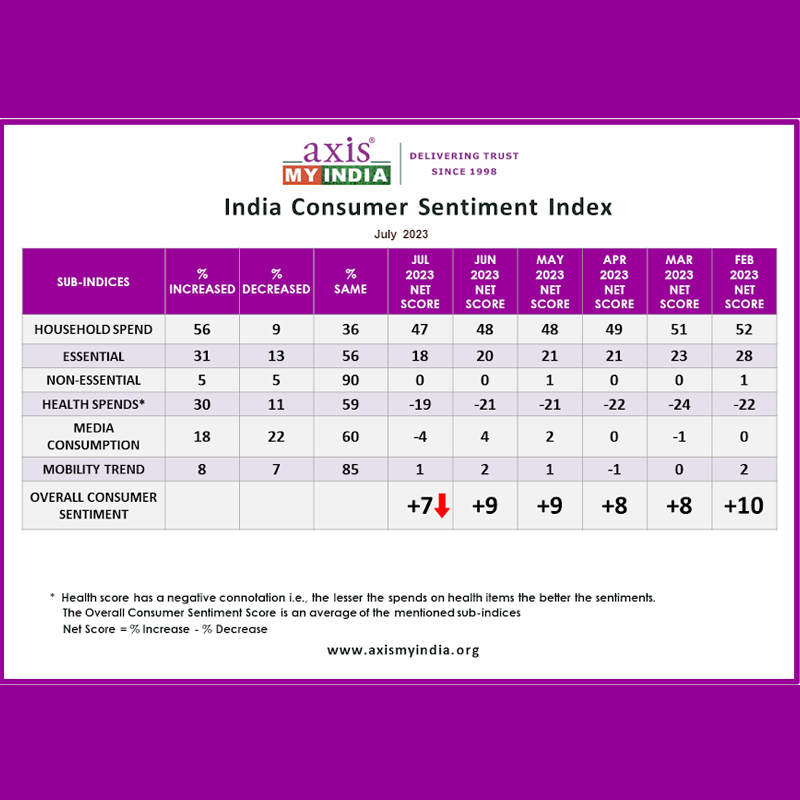

Mumbai: Axis My India, a consumer data intelligence company, has unveiled its latest report on the India Consumer Sentiment Index (CSI), providing invaluable insights into evolving media consumption patterns, consumer behaviour, and data privacy sentiments. The survey shows the change in media consumption, particularly among younger demographics, with TV News Channels and Social Media dominating as primary news sources. Moreover, the report reveals intriguing trends in movie theatre visits, online shopping habits, and preferred sources of product information. With data-driven observations and comprehensive analysis, this report serves as a crucial resource for businesses seeking to align their marketing strategies with changing consumer preferences in the digital age.The July net CSI score, calculated by percentage increase minus percentage decrease in sentiment, is at +7, which has decreased as compared to last month (+9).

The sentiment analysis delves into five relevant sub-indices – Overall household spending, spending on essential and non-essential items, spending on healthcare, media consumption habits, and entertainment & tourism trends.

The survey was carried out via Computer-Aided Telephonic Interviews with a sample size of 5072 people across 35 states and UTs. 67% belonged to rural India, while 33% belonged to urban counterparts. In terms of regional spread, 23% belong to the Northern parts while 22% belong to the Eastern parts of India. Moreover, 26% and 29% belonged to Western and Southern parts of India respectively. 59% of the respondents were male, while 41% were female. In terms of the two majority sample groups, 31% reflect the age group of 36YO to 50YO and 27% reflect the age group 26YO to 35YO.

Commenting on the CSI report, Axis My India chairman & MD Pradeep Gupta said, “Amidst India’s ever-changing economic landscape, our comprehensive survey reveals fascinating patterns in media consumption, information seeking, and online shopping habits. Embracing the digital era, the youth drive a surge in digital platform usage, while traditional sources like TV news maintain steadfast relevance. The cinema’s revival is noteworthy, with urbanites and seniors spearheading this trend. Trust remains paramount, as consumers rely on shopkeepers, local markets, and online searches for product insights. However, data privacy concerns loom, particularly among the younger generation. These insightful trends underscore the imperative for a versatile approach to cater to the diverse preferences of our dynamic consumer base.”

Key findings

. Overall household spending has increased for 56% of the families, which is the same as the last two months. The net score, which was +48 last month is +47 this month. The increase is slightly higher in rural households (57%).

. Spends on essentials like personal care & household items has increased for 31% of the families, which has decreased by 1% from last month. The net score, which was at +20 last month has dipped to +18 this month. Essential spends continue to increase majorly for the rural segment of the consumers (32%) and among 18-25-year-olds (38%).

. Spends on non-essential & discretionary products like AC, Car, and Refrigerators have increased for 5% of families, which is the same as last two months. The net score is 0, which was same as the last month.

. Expenses towards health-related items such as vitamins, tests, and healthy food has surged for 30% of families. This reflects a decrease in consumption by 2% from last month. The health score which has a negative connotation i.e., the lesser the spends on health items the better the sentiments, has a net score value -19 this month. Health-related products consumption increased more for the rural segment of the consumers (31%), among females (30%), and among those within the age group of 26-35-year-olds (34%).

. Consumption of media (TV, Internet, Radio, etc.) has increased for 18% of families, depicting a significant dip in increased media consumption percentage by 6% from last month. This decrease is depicted after an increase was reflected last month at 24% (the highest since April 23) majorly due to IPL. The overall, net score which was at +4 last month is at -4 this month. The increase in Media viewership percentage could be majorly reflected among males (20%) and 18-25 YO (29%) compared to older age groups.

. Mobility has increased for 8% of the families, which is the same as last month. The overall mobility net indicator score, which was at +2 last month, is at +1 this month. Mobility is highest amongst the age group of 18-25YO at 14% which is 2% more than last month for the same age group.

On topics of current national interest

. This month Axis My India CSI survey aimed to understand the primary platform that consumers rely on to stay updated with the latest news. As per the findings, TV News Channels are the primary news source for 44% of respondents, followed by Social Media (23%) and YouTube education/news channels (18%). Newspapers accounted for only 14% of news consumption, while YouTube Shorts had 7%. TV News Channels and Newspapers are preferred majorly by viewers above 60 years while social media platforms and formats are majorly preferred by 18-25YO.

. Another key aspect explored was the frequency of movie theatre visits in recent months. The findings reveal interesting patterns in consumer behaviour, where in out of all the respondents, 49% stated that they visited movie theatres once a month, 30% twice, 8% thrice, and 13% more than three times. As a significant proportion of consumers visit movie theatres at least once a month, it could be apt to assume that a consistent interest in cinema as a form of entertainment is again rising back. This keenness is majorly witnessed amongst urban consumers (51%), and females (57%).

. When seeking information about products they intend to buy, respondents in the Axis My India survey relied on various sources. The primary sources of information were shopkeepers and local markets (36%), followed closely by internet searches (29%), indicating the significance of both traditional and digital channels. A notable 19% of respondents preferred seeking advice from friends, colleagues, or neighbours, highlighting the continued influence of word-of-mouth recommendations in purchase decisions. YouTube emerged as a source of product information for 6% of respondents, demonstrating the growing popularity of video content in informing consumer choices and Television advertisements held relevance for 5% of respondents. Only 2% refer to social media, and 1% go directly to the company website or use print media. While those above 60 years old prefer shopkeepers and local markets, 18-25YO prefer internet searches and YouTube videos. The majority of the 51-60YO prefer seeking advice from others.

. The survey further unveiled a diverse range of online shopping habits among consumers with a sizable portion yet to adopt e-commerce as their preferred mode of shopping. A significant 64% stated they never shop online. However, 11% do online shopping once a month, and 7% do so once in 6 months to 1 year. Additionally, 6% shopped online once in the last 6 months, and another 6% did so more than once in the last month. Only 3% shopped online more than once in the last 6 months, while a mere 2% engaged in online shopping almost every week. 18-25YO forms the majority segment that shops once a month (19%).

. The survey further gauged respondents’ sentiments regarding data privacy and security in the context of the increasing usage of the internet and technology in their daily lives. The findings reveal that 45% of respondents reported not being worried about data privacy and security, while 23% expressed a significant concern. Additionally, 26% reported being worried to some extent suggesting a moderate level of concern about data privacy and security. They may have a general awareness of the risks involved but may not be overly alarmed by them. A majority of 18-35YO reflect apprehension to a large extent.

. Finally, the survey also focussed on farmers’ concerns about the potential repercussions of sdeficient monsoon on their farming activities in the current year. The findings revealed that 55% of farmers were highly worried, 24% expressed mild concern, 9% were optimistic about a good monsoon, and 13% expected normal monsoons. These findings highlight the apprehensions of a significant portion of farmers, emphasizing the importance of addressing agricultural challenges and potential risks associated with monsoon variability.

Digital

Content India 2026 opens with a copro pitch, a spice evangelist and a £10,000 prize for Indian storytelling

Dish TV and C21Media’s three-day summit puts seven ambitious projects before an international jury, and two walk away with serious development money

MUMBAI: India’s content industry gathered in Mumbai this March for Content India 2026, a three-day summit organised by Dish TV in partnership with C21Media, and it wasted no time making a statement. The event opened with a Copro Pitch that put seven scripted and unscripted television concepts before an international panel of judges, and by the end of it, two projects had walked away with £10,000 each in marketing prize money from C21Media to support development and international promotion.

The jury, comprising Frank Spotnitz, Fiona Campbell, Rashmi Bajpai, Bal Samra and Rachel Glaister, evaluated a shortlist that ranged from a dark Mumbai comedy-drama about mental health (Dirty Minds, created by Sundar Aaron) to a Delhi coming-of-age mystery (Djinn Patrol, by Neha Sharma and Kilian Irwin), a techno-thriller about a teenage gaming prodigy (Kanpur X Satori, by Suchita Bhatia), an investigative crime drama blending mythology and modern thriller (The Age of Kali, by Shivani Bhatija), a documentary on India’s spice heritage (The Masala Quest, hosted by Sarina Kamini), a documentary on competitive gaming (Respawn: India’s Esports Revolution, by George Mangala Thomas and Sangram Mawari), and a reality-horror competition merging gaming and immersive fear (Scary Goose, by Samar Iqbal).

The session was hosted by Mayank Shekhar.

The two winners were Djinn Patrol, backed by Miura Kite, formerly of Participant Media and known for Chinatown and Keep Sweet: Pray & Obey, with Jaya Entertainment, producers of Real Kashmir Football Club, also attached; and The Masala Quest, created and hosted by Sarina Kamini, an Indian-Australian cook, author and self-described “spice evangelist.”

The summit also unveiled the Content India Trends Report, whose findings made for bracing reading. Daoud Jackson, senior analyst at OMDIA, set the tone: “By 2030, online video in India will nearly double the revenue of traditional TV, becoming the main driver of growth.” He noted that in 2025, India produced a quarter of all YouTube videos globally, overtaking the United States, while Indians collectively spend 117 years daily on YouTube and 72 years on Instagram. Traditional subscription TV is declining as free TV and connected TV gain ground, forcing broadcasters to innovate. “AI-generated content is just 2 per cent of engagement,” Jackson added, “highlighting the dominance of high-quality human content. The key for Indian media companies is scaling while monetising effectively from day one.”

Hannah Walsh, principal analyst at Ampere Analysis, added hard numbers to the picture. India produced over 24,000 titles in January 2026 alone, with 19,000 available internationally. The country now accounts for 12 per cent of Asia-Pacific content spend, up from 8 per cent in 2021, outpacing both Japan and China. Key exporters include JioStar, Zee Entertainment, Sony India, Amazon and Netflix, delivering over 7,500 Indian-produced titles abroad each year. The top importing markets are Saudi Arabia, the UAE, Egypt, the United States and the Philippines. Scripted content dominates globally at 88 per cent, with crime dramas and children’s and family titles performing particularly strongly.

Manoj Dobhal, chief executive and executive director of Dish TV India, framed the summit’s ambition squarely. “Stories don’t need translation. They need a platform, discovery, and reach, local or global,” he said. “India produces more movies than any country, our streaming platforms compete globally, and our tech and creators win international awards. Yet fragmentation slows growth. Producers, platforms, and tech move in different lanes. We need shared spaces, collaboration, and an ecosystem where ideas, technology, and people meet. That is why we built Content India.”

The data, the pitches and the prize money all pointed to the same conclusion: India is not waiting for the world to discover its stories. It is building the infrastructure to sell them.