AD Agencies

Havas hits the accelerator as AI strategy bears fruit

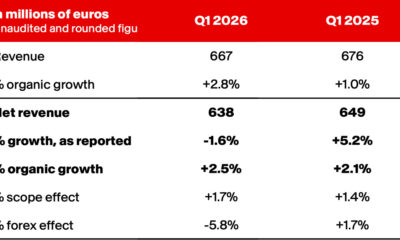

PARIS: Havas is charging into the final quarter of 2025 with a spring in its step. The advertising group posted organic net revenue growth of 3.8 per cent in the third quarter, smashing expectations and vindicating its strategic pivot towards artificial intelligence and data-driven marketing. The surge in top-line performance prompted management to sharpen full-year guidance decisively upwards, signalling confidence that the worst of the economic headwinds facing the sector have passed.

The results reveal a business in motion. North America blazed a trail with organic growth of 7.4 per cent, driven chiefly by Havas Health’s double-digit expansion and its ability to wring higher budgets out of existing clients—a rare feat in an industry where money typically flows only to new business wins. The Asia-Pacific region bounced back smartly from a tepid second quarter with 8.2 per cent growth, whilst the United Kingdom performed solidly. France, dragged down by a tough comparison with last year’s Olympic Games boost, and Latin America, battered by unfavourable currency moves, were the laggards.

Havas now expects full-year net revenue organic growth of between 2.5 and 3.0 per cent, up from previous guidance of above 2.0 per cent. More significantly, the group reckons on an adjusted EBIT margin improvement of around 50 basis points to approximately 12.9 per cent—a meaningful lift that suggests operational leverage is kicking in. The nine-month figures show organic growth of 2.8 per cent, buoyed by cross-selling wins amongst the top 30 clients.

The financial picture is straightforward: Havas is extracting better returns from its existing client base whilst simultaneously expanding its footprint. Operating margin expansion of this magnitude rarely happens by accident. The group has plainly succeeded in persuading clients to spend more on higher-margin services and shifted work into more profitable lines—precisely what a well-functioning agency should accomplish.

Two strategic moves underscore management’s ambition. The majority acquisition of Tidart, a Spanish digital performance specialist, plugs gaps in Havas’ capabilities across e-commerce and performance marketing. More consequential is the formation of Horizon Global, a joint venture with Horizon Media Holdings worth a combined $20 billion in global billings. Styled as an “AI-native solution,” the venture signals that Havas’ Converged.AI strategy—the group’s bet on helping clients harness artificial intelligence across their marketing ecosystems—is moving from rhetoric into revenue-generating reality.

Chief executive vYannick Bolloré spoke of “impressive commercial momentum” and “notable new business wins.” Translation: the market is buying what Havas is selling.

None of this occurs in a vacuum. Foreign exchange movements clipped 3.9 per cent from reported revenue growth, with the dollar’s recent weakness particularly stinging. Geopolitical tensions, trade pressures and political uncertainties lurk in the background. The group remains cautious about the year ahead, even as it tightens guidance.

The broader picture for Havas: a global advertising industry grinding through modest growth and relentless margin pressure is being challenged—and beaten—by a group that has successfully positioned itself as a challenger taking share through genuine commercial innovation. Whether that momentum persists through 2026 is the question investors are asking now. For the moment, the trajectory looks encouraging.